As we prepare this commentary, it is a wet and cold Sydney morning like many we’ve had to bear this year. Days like these serve as a reminder that sunshine is not a guarantee and every now and then we must endure periods of rain and gloom. Like financial markets, we seem to be going through a wet patch and as much as it makes our portfolio dark and deary, we know sooner or later the sun will shine again.

What a year 2022 has been. Just as we emerge out of lock down and learn to live with the pandemic, we are confronted with the Russian invasion of Ukraine, causing more supply-side issues and pushing inflation higher. When we talk to statisticians, they term COVID19 and the Ukraine invasion as a 1 in 100-year event…and yet, we have had two of these events in the last three years.

For the first time in a long time, we saw a positive correlation between equities and bonds as both growth and defensive assets fell. What we found most interesting was that through this period, GDP growth remained positive and labour markets are now stronger than they have ever been compared to the last 15 years.

Figure 1: Asset Class Performance Over 3 Months and 1-Year to June 2022

Source: Allied Wealth, Morningstar

Analysing data points and market themes, what stands out today is the outsized impact central banks have on financial markets. Whilst media pundits would point to inflation or animal spirits, our considered view remains that central banks, more specifically the reaction of central bankers to economic conditions, have been the primary drivers of market performance during 2022.

Alongside quantitative easing, central banks have one other significant tool in their kit which is the ability to adjust cash rates (referred to as Monetary Policy), and this in turn affects everything from borrowing costs to corporate behaviour. Unfortunately, this very blunt instrument is being used to solve a myriad of complex market problems.

Much like an axe, monetary policy is much better used to chop down the tree of aggregate demand than it is to kill the flies of inflation, especially when recent prints have been largely driven by supply-side issues. Whilst a fly swatter may be better, the only tool central bankers have is an axe, so markets are justifiably concerned about the precision of policy makers.

The blunt nature of monetary policy has resulted in an increase in market uncertainty for both equity and bond investors leading to the broader sell off. Equity investors are unclear what the net flow-through impact may be on company earnings whilst bond investors have seen their portfolios reprice lower as interest rates rose (the value of the bond inversely relates with higher interest rates – therefore meaning lower bond valuation).

More recent economic data points show that economic growth is moderating, but it remains too early to tell. There are also signs that supply chains have begun to recover for the second time, but timeframes vary greatly from industry to industry. At this point we could keep going on about the broad range of expected outcomes, possibilities and probabilities. However, as much as this may be an interesting thought exercise, the key question remains: where to from here?

What Can We Say More Definitively?

Based on a broad range of outcomes, taking a position on a short-term basis is a fool’s game as there does not seem to be sufficient information to form a short-term investment conviction. It is more likely that contradictory economic data will emerge leading to wild swings in asset prices a.k.a. market volatility.

Rather than a short horizon, a longer-term focus remains the smarter choice.

From a long-term perspective:

What Does This Mean for Our Portfolios?

Given where equity valuations sit relative to the long-term expected growth, we feel the probability and magnitude of return upside is much larger than the downside. Despite the lower probability, downside concerns have tempered the sizing of our risk-on allocation. Thus, we have proposed and implemented a marginal growth bias across all risk models. We will be looking to increase this risk-on position as more supportive economic data emerges.

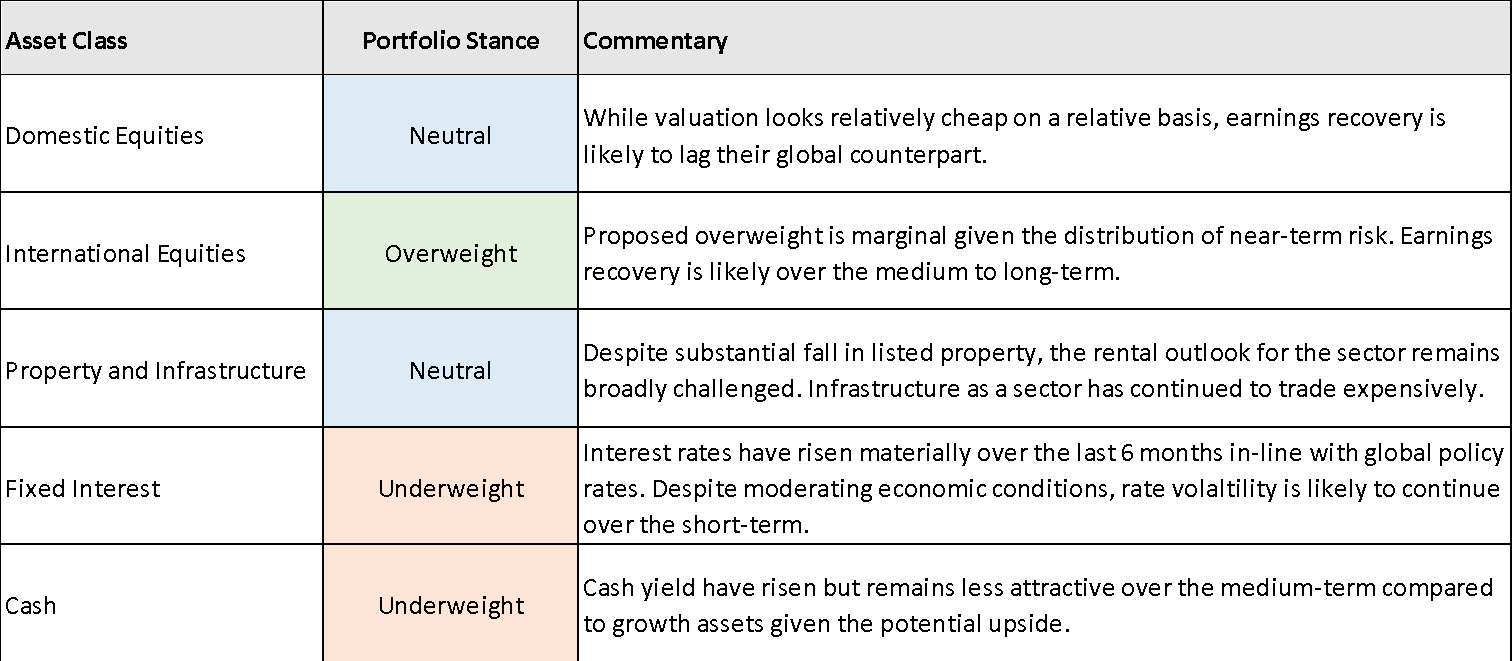

Figure 2: Asset Class Summary and Portfolio Stance

Note: Summary has been provided on an asset class basis. Please discuss actual asset allocations with your adviser as they may vary from model to model based on portfolio construction.

Rising inflation, the expectation of central bank rate hikes and the ongoing war in the Ukraine saw investors globally become more risk adverse during 2022. However, the companies that fell the most were typically expensive high price to earnings (PE) companies, anything related to crypto, tech companies or loss-making companies with unproven business models. All types of companies avoided by the Allied Portfolio’s Australian Equity investment process.

Additionally, 2022 has been a tough period for high priced tech stocks that generally have minimal to no earnings today, but the promise of large profits in the distant future. However, this always assumes that management’s grand plans are not disrupted. In an environment of close to zero interest rates, investors are willing to pay very high prices for large distant future profits, which have a present high value when discounted using a rate close to zero.

Rising rates make ‘boring’ profits and dividends of companies such as Amcor, Ampol and Transurban look more attractive than a tech company promising large ‘blue sky’ cash flow in 20 years’ time. This occurs as the present value of profits delivered today or next year are worth more than profits that may be generated in 10 of 15 years’ time.

Historically rising interest rates have diverted household expenditure from non-discretionary areas such as restaurants, travel and purchases of consumer goods to servicing mortgages. However, the tightening cycle in 2022 will look different to previous tightening cycles due to the potential bigger influence of fixed mortgages.

Companies that are adversely affected by rising rates are those in the consumer discretionary area, such as Myer, Flight Centre and Wesfarmers. Supermarkets and liquor retailers such as Coles, Endeavour and Woolworths tend to see a bounce from increases in dining at home & food inflation. Gambling stocks such as Tabcorp and the Lottery Company theoretically should see falling earnings, though historically that has not been the case, which says something about the foibles of Australians.

On the positive side, financials such as banks and insurance companies tend to do well in rising interest rate markets which sees higher profit margins. Banks will benefit from rising rates due to expanding net interest margins, less obvious beneficiaries are the insurance companies. For example, QBE holds an insurance float of US$29 billion. This ‘float’ incurs premiums paid upfront with claims paid out years later, with this bucket of cash being constantly replenished. Insurance companies are required to mostly hold their investments in high-quality government and corporate bonds as well as short term money market instruments, generally in the geographic area of insurance.

This has seen QBE's shareholders receive a minuscule return on this float for the past decade, with 1% earned in 2021 as interest rates were at historic lows in the USA, Europe and Australia. Rising interest rates combined with a hardening insurance market will see a significant expansion in investment earnings for QBE along with all insurers.

Less intuitive are utilities like Transurban, which you would think would do poorly in a rising rate environment due to their high level of interest costs. However due to long term hedged cost debt with a maturity close to 8 years and toll escalators linked to inflation; Transurban will see an estimated $50M per annum benefit over the next 4 years from every 1% increase in inflation.

The Allied Wealth Investment Committee are pleased with how the Portfolio is positioned, every company is profitable, sensibly geared or in several cases has no debt and every company pays a dividend. During times of market stress and rising interest rates, companies that pay a steady dividend that is growing ahead of inflation provide an airbag not enjoyed by loss-making companies and 'concept stocks' promising vast profits in the distant future.

Finally, this winter has shaped up to be one of the least enjoyable ones for some years. This sentiment is further compounded by a particularly bad flu season and virulent COVID19 strains. I hope everyone keeps well through this season.

We look forward to speaking to you again soon. In the meantime, if you have any questions about this commentary or your portfolio your adviser will be very happy to help.

Yours faithfully,

Allied Wealth Investment Committee