Unlike the past few bank reporting seasons, there was little trepidation from investors going into the November 2025 bank reporting season. The last few bank reporting seasons have been very consistent, with a similar story of high margins, solid loan growth, strong capital, and minimal bad debts. An excellent position for investors with a large weighting to the banks but infuriating for professional fund managers who sold down their bank exposures in early 2024 due to concerns about recession, rising bad debts, and valuation concerns, particularly in the case of the Commonwealth Bank.

In this piece, we look at the major themes played out over the November 2025 bank reporting season. Even for investors that don't own the banks, looking closely at their results provides a window into the financial health of Australia. Overall, we were happy with the banks held in the Allied Portfolio.

The banks, including Macquarie, currently make up 27% of the ASX and is the largest sector on the ASX, significantly higher than miners at 18%. The sector has been the one of the better performing sectors on the ASX in 2025 +14%, ahead of the ASX 200 +9%, though the lead has been pared back since July due to the fall in CBA off -19% since the start of July.

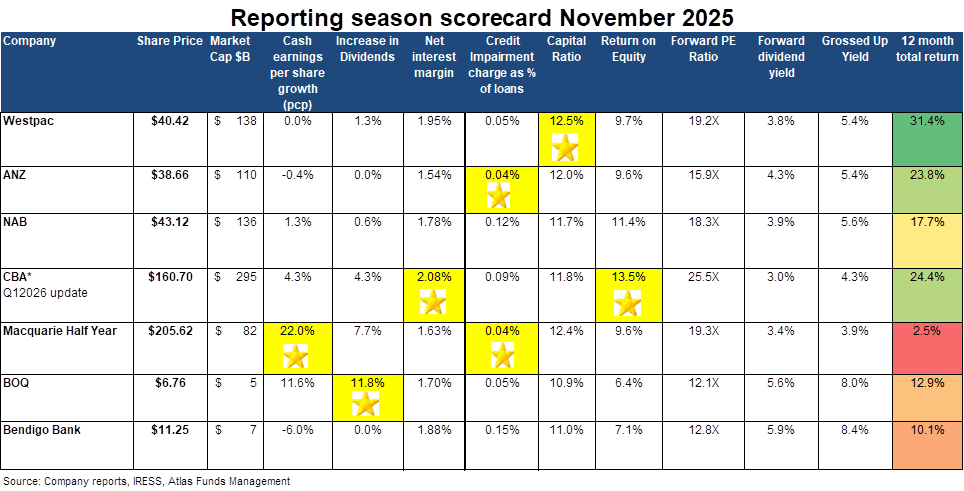

Bad debts remained low throughout 2025, with all banks reporting extremely low loan losses. ANZ and Macquarie reported the lowest bad debts at 0.04% of gross loans, reflecting the continued discipline of banks in not writing loans at any cost. Across the rest of the banks, none reported bad debts exceeding 0.15% of gross loans.

The level of loan losses is important for investors, as high loan losses reduce profits and, consequently, lower dividends due to the resulting lower bank capital base. This reporting season has seen low bad debts translated into better-than-expected profits and, thus, higher dividends.

Bad debts remained low in 2025, with all banks reporting negligible loan losses; Westpac, Macquarie and ANZ reported the lowest level, with loan losses of 0.04%. To put this in context, after the 1992 recession, bank loan losses have averaged around 0.30% of outstanding loans, and banks price loans assuming losses of this magnitude. Similarly, sell-side analysts issue share price targets on the banks, assuming a reversion in losses at this level. We believe the loans to developers, property syndicates and troubled industrial companies that are impaired now sit with non-bank lenders and private debt funds rather than the big four banks.

In the November 2025 bank reporting season, the banks announced smaller increases in dividends than we have seen over the last few years, with the average dividend increase across the big banks being 1%. Macquarie Bank had the largest dividend increase of 8%, with ANZ at the other end, holding the dividend the same as they did last year.

Interestingly ANZ not cutting the dividend was probably one of the bigger pieces of news in the reporting season, with the consensus view being that ANZ’s new CEO would adopt the traditional playbook of an incoming CEO – blame previous management for errors, increase provisions and cut the dividend to “preserve capital” – thus allowing the CEO to look good in future years as the provisions are written back (boosting reported profits) and the dividend increased.

Pleasingly ANZ’s CEO announced a cost-cutting exercise and kept the dividend saying that the bank was in good shape, this saw the share price bounce 10%.

Franking account balances in the banks remain very strong with CBA sitting at $2B in excess credits, Westpac is still the leader with $3.7B as a consequence of not paying an interim dividend in 2020 and being slower to pay full dividends coming out of CV-19. Bank investors can look forward to a solid stream of franked dividends for the foreseeable future. Indeed, the franking balances in the banks are likely to build further in coming years with the retirement of hybrids, many banks had used hybrids as a means to stream out excess franking credits.

In 2025, the Australian banks are all very well capitalised and have seen their capital build. This enables banks to return capital to shareholders through on-market buybacks and increased dividend payments. While the banks have not been actively buying back their shares recently, the ongoing buybacks serve as a sort of floor in the share price, with the banks stepping back into the market to purchase shares when the share price falls below a certain threshold. Indeed, CBA's $1 billion market buyback last bought back a share on November 15, 2024, at $151 per share.

Overall, we are happy with the financial results from the banks owned by the Allied Australian Equity Portfolio in November. Westpac, ANZ and Macquarie either maintained or increased their dividends, with the market expecting ANZ's new CEO to usher in a rebasing of the dividend lower.

All banks demonstrated solid net interest margins, low non-performing loans, and effective cost control. In 2026, the banks will all have cleaner loan books, more consistent earnings and a greater margin of safety than they have had in the past.

In a turbulent world with weekly changes in trade policies, Australia's major banks are likely to continue positively surprising the market, operating in a small oligopolistic market, sheltered from both new competition and global storms. Allied Wealth has been more optimistic towards the banks than most over the past few years, which has been positive for our investors. However, given current valuations and portfolio construction constraints, we are likely to reduce our holdings and would need CBA to fall more before we bought back the stock we sold earlier on in 2025.