Whilst the seasons might be changing, for financial markets it was more or less the same. Themes discussed in the last newsletter remain dominant today – we sound a bit like a broken record repeating ourselves.

Central banks and their actions continue to wield an outsized influence on the direction of equity, bond, and currency markets. Over the quarter, asset allocation performance has been flat relative to the strategic asset allocation. Size of positions were small in-line with the cautiously positive overall outlook.

Figure 1: Allied Wealth Asset Allocation Performance – 3-Months to 30th September 2022

| 3-Months to 30th Sept 2022 | Moderate | Balanced | Growth | High Growth |

| Asset Allocation | -1.6 | -1.7 | -1.8 | -1.9 |

| Strategic Asset Allocation | -1.6 | -1.7 | -1.8 | -1.8 |

| Excess Return | 0.0 | 0.0 | 0.0 | -0.1 |

Source: Allied Wealth, Morningstar

Performance over the September quarter was characterised by a strong equity market rally in the first half followed by a fall in the second half. What stood out overall was the strength of the US dollar relative to most developed market currencies, which supported the relative outperformance of unhedged relative to hedged international equities.

Figure 2: Asset Class Performance as at 30th September 2022

Source: Allied Wealth, Morningstar

On the economic front, more data points have emerged to suggest that aggregate demand is softening, while higher interest rates have started to weigh on consumer and corporate spending.

Supply chain disruptions and the energy crisis, which were major themes early this year, have started to rectify themselves. Cost of shipping has fallen since the start of the year, while factory manufacturing activity has slowed. Natural gas prices have been volatile but current levels are much lower compared to previous peaks.

Figure 3: Natural Gas Prices in USD 2022 Year-to-Date

Labour conditions remain robust, but we believe it is a matter of time before the reduction in demand translates into weaker wage growth. As with all these data points, timing is the greatest uncertainty!

As the song goes – Why Can’t We Be Friends?

Putting aside economic indicators, we highlight longer-term structural trends from the evolution of the US-China relationship. So far into 2022, the US government has imposed further trade restrictions (on China), particularly as they relate to technology exports forcing a growing divide between global companies choosing to work closer with China, or with the US.

Over the quarter, we observed on-shoring or friend-shoring activity (mostly relocation of factories away from China to the US or jurisdictions friendly to the US) as companies look to build out supply chains more resilient to geopolitical risks.

Consequently, China has experienced a substantial outflow of foreign capital. Discussions with asset owners and managers indicate majority of remaining investments in China today reflect opportunistic positions rather than core long-term holdings. We are not surprised by this given the success of Xi Jin Ping in consolidating power and winning a precedent-breaking third term as party leader. The world is bracing for further escalation of geopolitical conflict.

What Does This Mean for Our Portfolios?

Developed market central banks have continued to tighten monetary policy. At the current pace we see an increased probability of a recessionary scenario as bankers have focused primarily on headline inflation. Equity market valuations look attractive on a historical basis – equity markets have generally fallen in-line with changing expectations of interest rates.

China whilst still considered a large part of the global growth engine, is expected to play a reduced role over the longer term. We expect to see other countries benefit from this and in turn should lead to a more diversified global growth profile.

Liquidity conditions have continued to tighten due to a combination of higher debt costs (reducing transaction volumes) and reticence of asset owners to deploy capital into a volatile market.

Over the long-term, we continue to expect earnings recovery as companies readjust to more challenging market conditions. Over the short-to-medium term, we see a situation where a mild recession triggered by central banks are met with static monetary policy as bankers look to retain ammunition against future systemic risk events.

In-line with this view, we retain the marginal growth bias across all risk models. Positions today remain appropriately sized given the range of expected outcomes both on the upside and downside.

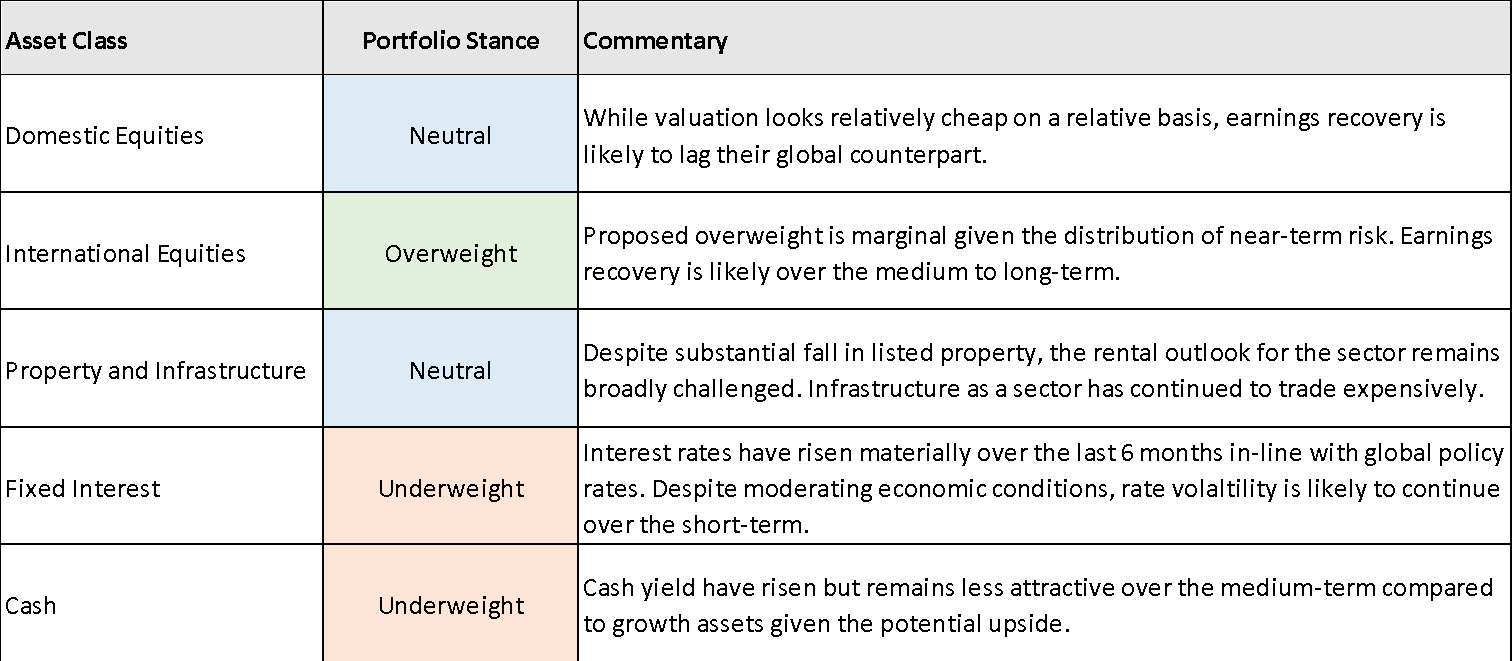

Figure 4: Asset Class Summary and Portfolio Stance

| Asset Class | Portfolio Stance | Commentary |

| Domestic Equities | Neutral | Valuation continues to look cheap. Asset class has been supported by the slower pace of monetary policy as well as a substantially weaker AUD (relative to USD). |

| International Equities | Overweight | Proposed overweight is marginal given the distribution of near-term risk. Earnings recovery is likely over the medium to long-term. |

| Property and Infrastructure | Neutral | Rental outlook for the sector remains broadly challenged, particularly for the Retail and Office sector. Industrial property continues to trade expensively in contradiction to the reduction in demand. Infrastructure as a sector has continued to trade expensively. |

| Fixed Interest | Underweight | Interest rates have risen materially over the year-to-date in-line with global policy rates. Economic conditions have moderated further, although market uncertainty around terminal rates implies that rate volatility is likely to continue over the short-term. |

| Cash | Underweight | Cash yield have risen but remains less attractive over the medium-term compared to growth assets given the potential upside. |

Bottom-Up Market Observations

Over the next twelve months, we expect that the two key factors driving equity markets will be rising interest rates and a weaker Australian dollar, both of which will be positive for many of the companies in the Portfolio.

This year we saw the end of near-zero interest rates, unprecedented over the past five thousand years of human commercial transactions, below previous low points of 4% in Ancient Rome in 1 AD and 1.12% from the Republic of Genoa in 1619! Rising or, more accurately, normalizing of interest rates will present a challenge for many newly listed tech companies. Often these companies have business models that require low-interest rates, accommodating bankers and equity markets willing to finance losses.

This year has been a tough for high-priced tech stocks with minimal to no earnings today and only the promise of large profits in the distant future. In an environment of close to zero interest rates, investors are willing to pay very high prices for large distant future profits, which have a present high value when discounted using a rate close to zero.

Rising rates make the “boring” profits and dividends of companies such as Amcor, Ampol and Transurban look more attractive than a tech company promising large “blue sky” cash flow in 20 years. This occurs as the present value of profits delivered today or next year are worth more than profits that may be generated in 10 of 15 years.

Additionally, the Portfolio is constructed to be well hedged against rising interest rates due to either earnings being linked to increasing rates or the company having pricing power to pass on higher costs to their customers. Our positions in insurance companies, toll roads and banks will benefit from rising interest rates.

One factor that is currently being ignored by the market is the impact of a falling Australian Dollar. Over the past year, the AUD has declined by 16% against the USD to sit at US 64 cents. The last time that the AUD was consistently at this level was in early 2009. While this is bad news for those planning ski holidays in Colorado at Christmas, it is good news for many companies in the Portfolio that either have significant operations outside of Australia, or export goods that are sold in USD with costs incurred in AUD. For example, chemical company Incitec Pivot benefits from a falling AUD in two ways. Firstly, the profits Incitec earns in the USA from selling ammonia and explosives are now worth more when translated into Australian Dollars. Secondly, the fertilizer that Incitec manufactures in Australia is priced to compete with imports. A falling AUD makes imported fertilizer more expensive, thus allowing the company to increase their prices and expand their profit margins.

Currently, around 44% of profits generated in the Portfolio will see a positive impact from a falling AUD, with the bulk of these profits earning in USD. Suppose the current weakness in the AUD is maintained. In that case, Atlas expects a significant increase in AUD-reported profits and AUD dividends for the companies held in the Portfolio in the February 2023 reporting season. This occurs because one US dollar of earnings has increased by 16% for Australian-domiciled investors.

May the odds be ever in your favour! It’s been an exciting Melbourne Cup week and the race has left us with great memories but lighter pockets!

Yours faithfully,

Allied Wealth Investment Committee

As we prepare this commentary, it is a wet and cold Sydney morning like many we’ve had to bear this year. Days like these serve as a reminder that sunshine is not a guarantee and every now and then we must endure periods of rain and gloom. Like financial markets, we seem to be going through a wet patch and as much as it makes our portfolio dark and deary, we know sooner or later the sun will shine again.

What a year 2022 has been. Just as we emerge out of lock down and learn to live with the pandemic, we are confronted with the Russian invasion of Ukraine, causing more supply-side issues and pushing inflation higher. When we talk to statisticians, they term COVID19 and the Ukraine invasion as a 1 in 100-year event…and yet, we have had two of these events in the last three years.

For the first time in a long time, we saw a positive correlation between equities and bonds as both growth and defensive assets fell. What we found most interesting was that through this period, GDP growth remained positive and labour markets are now stronger than they have ever been compared to the last 15 years.

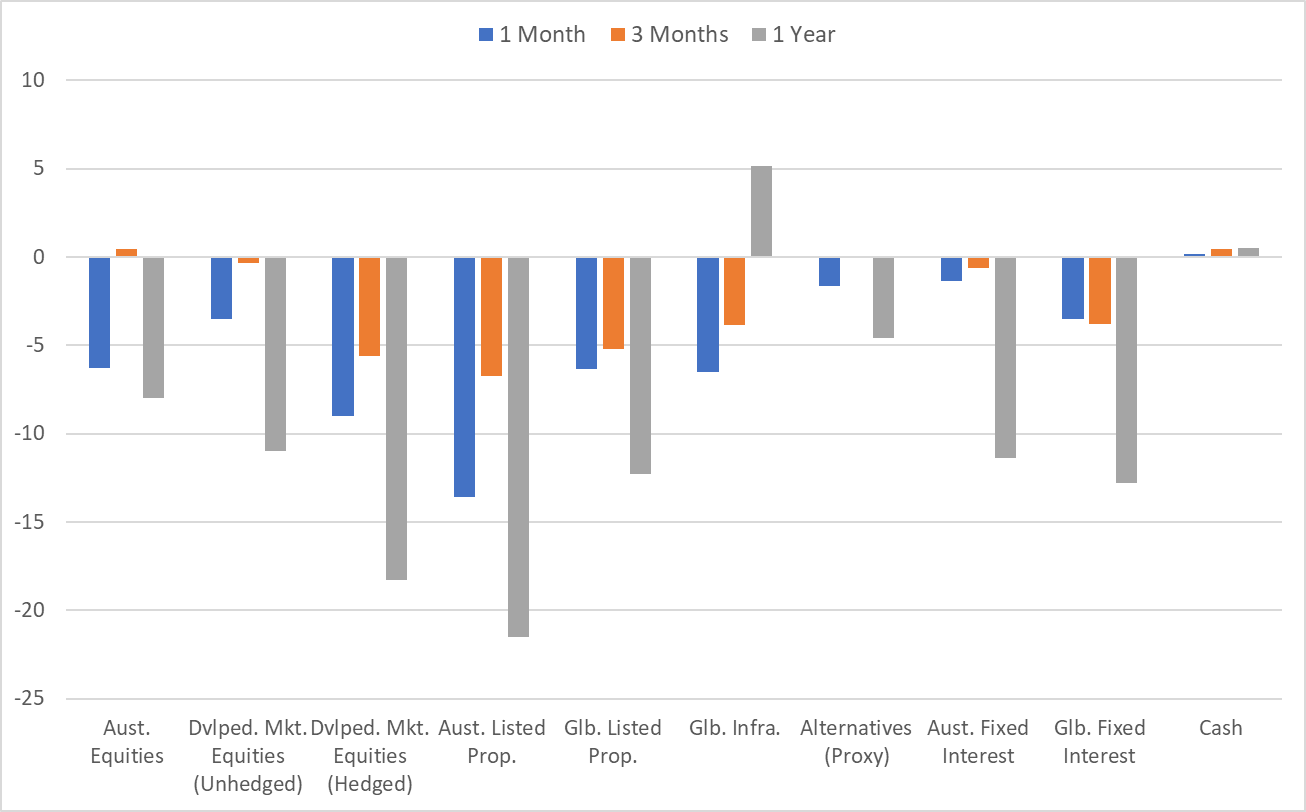

Figure 1: Asset Class Performance Over 3 Months and 1-Year to June 2022

Source: Allied Wealth, Morningstar

Analysing data points and market themes, what stands out today is the outsized impact central banks have on financial markets. Whilst media pundits would point to inflation or animal spirits, our considered view remains that central banks, more specifically the reaction of central bankers to economic conditions, have been the primary drivers of market performance during 2022.

Alongside quantitative easing, central banks have one other significant tool in their kit which is the ability to adjust cash rates (referred to as Monetary Policy), and this in turn affects everything from borrowing costs to corporate behaviour. Unfortunately, this very blunt instrument is being used to solve a myriad of complex market problems.

Much like an axe, monetary policy is much better used to chop down the tree of aggregate demand than it is to kill the flies of inflation, especially when recent prints have been largely driven by supply-side issues. Whilst a fly swatter may be better, the only tool central bankers have is an axe, so markets are justifiably concerned about the precision of policy makers.

The blunt nature of monetary policy has resulted in an increase in market uncertainty for both equity and bond investors leading to the broader sell off. Equity investors are unclear what the net flow-through impact may be on company earnings whilst bond investors have seen their portfolios reprice lower as interest rates rose (the value of the bond inversely relates with higher interest rates – therefore meaning lower bond valuation).

More recent economic data points show that economic growth is moderating, but it remains too early to tell. There are also signs that supply chains have begun to recover for the second time, but timeframes vary greatly from industry to industry. At this point we could keep going on about the broad range of expected outcomes, possibilities and probabilities. However, as much as this may be an interesting thought exercise, the key question remains: where to from here?

What Can We Say More Definitively?

Based on a broad range of outcomes, taking a position on a short-term basis is a fool’s game as there does not seem to be sufficient information to form a short-term investment conviction. It is more likely that contradictory economic data will emerge leading to wild swings in asset prices a.k.a. market volatility.

Rather than a short horizon, a longer-term focus remains the smarter choice.

From a long-term perspective:

What Does This Mean for Our Portfolios?

Given where equity valuations sit relative to the long-term expected growth, we feel the probability and magnitude of return upside is much larger than the downside. Despite the lower probability, downside concerns have tempered the sizing of our risk-on allocation. Thus, we have proposed and implemented a marginal growth bias across all risk models. We will be looking to increase this risk-on position as more supportive economic data emerges.

Figure 2: Asset Class Summary and Portfolio Stance

Note: Summary has been provided on an asset class basis. Please discuss actual asset allocations with your adviser as they may vary from model to model based on portfolio construction.

Rising inflation, the expectation of central bank rate hikes and the ongoing war in the Ukraine saw investors globally become more risk adverse during 2022. However, the companies that fell the most were typically expensive high price to earnings (PE) companies, anything related to crypto, tech companies or loss-making companies with unproven business models. All types of companies avoided by the Allied Portfolio’s Australian Equity investment process.

Additionally, 2022 has been a tough period for high priced tech stocks that generally have minimal to no earnings today, but the promise of large profits in the distant future. However, this always assumes that management’s grand plans are not disrupted. In an environment of close to zero interest rates, investors are willing to pay very high prices for large distant future profits, which have a present high value when discounted using a rate close to zero.

Rising rates make ‘boring’ profits and dividends of companies such as Amcor, Ampol and Transurban look more attractive than a tech company promising large ‘blue sky’ cash flow in 20 years’ time. This occurs as the present value of profits delivered today or next year are worth more than profits that may be generated in 10 of 15 years’ time.

Historically rising interest rates have diverted household expenditure from non-discretionary areas such as restaurants, travel and purchases of consumer goods to servicing mortgages. However, the tightening cycle in 2022 will look different to previous tightening cycles due to the potential bigger influence of fixed mortgages.

Companies that are adversely affected by rising rates are those in the consumer discretionary area, such as Myer, Flight Centre and Wesfarmers. Supermarkets and liquor retailers such as Coles, Endeavour and Woolworths tend to see a bounce from increases in dining at home & food inflation. Gambling stocks such as Tabcorp and the Lottery Company theoretically should see falling earnings, though historically that has not been the case, which says something about the foibles of Australians.

On the positive side, financials such as banks and insurance companies tend to do well in rising interest rate markets which sees higher profit margins. Banks will benefit from rising rates due to expanding net interest margins, less obvious beneficiaries are the insurance companies. For example, QBE holds an insurance float of US$29 billion. This ‘float’ incurs premiums paid upfront with claims paid out years later, with this bucket of cash being constantly replenished. Insurance companies are required to mostly hold their investments in high-quality government and corporate bonds as well as short term money market instruments, generally in the geographic area of insurance.

This has seen QBE's shareholders receive a minuscule return on this float for the past decade, with 1% earned in 2021 as interest rates were at historic lows in the USA, Europe and Australia. Rising interest rates combined with a hardening insurance market will see a significant expansion in investment earnings for QBE along with all insurers.

Less intuitive are utilities like Transurban, which you would think would do poorly in a rising rate environment due to their high level of interest costs. However due to long term hedged cost debt with a maturity close to 8 years and toll escalators linked to inflation; Transurban will see an estimated $50M per annum benefit over the next 4 years from every 1% increase in inflation.

The Allied Wealth Investment Committee are pleased with how the Portfolio is positioned, every company is profitable, sensibly geared or in several cases has no debt and every company pays a dividend. During times of market stress and rising interest rates, companies that pay a steady dividend that is growing ahead of inflation provide an airbag not enjoyed by loss-making companies and 'concept stocks' promising vast profits in the distant future.

Finally, this winter has shaped up to be one of the least enjoyable ones for some years. This sentiment is further compounded by a particularly bad flu season and virulent COVID19 strains. I hope everyone keeps well through this season.

We look forward to speaking to you again soon. In the meantime, if you have any questions about this commentary or your portfolio your adviser will be very happy to help.

Yours faithfully,

Allied Wealth Investment Committee