This paper includes new policy initiatives announced on Budget Night of 12 May 2026.

Item | Description | Impact | ||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Taxation | ||||||||||||||||||||||||

1. Capital Gains Tax (CGT) Changes Effective: 1 July 2027 | The 50% CGT discount will be replaced by a return to CPI indexation from 1 July 2027 together with the introduction of a minimum tax rate of 30 per cent on realised gains. This will apply to all assets except new homes, where both new and old arrangements will be available. The replacement of the CGT discount will be prospective, with gains accrued on existing investments prior to the start date to retain the 50 per cent discount. Investors can seek a valuation as at 30 June 2027 or use an estimate as supported by ATO tools. The 30% minimum tax on real capital gains applies to assets held by individuals, trusts and partnerships. Pre 1985 CGT assets will not be exempt, with gains from 1 July 2027 taxed. | Superannuation funds and companies are exempt and are major beneficiaries of the changes. Investors, especially retirees, may lean more towards investments that provide a higher proportion of income especially franked dividends. The strategy of deferring the realisation of capital gains until after retirement will become less effective. Individuals to consider bringing forward some capital gains before the minimum tax rate of 30% comes into effect. Individuals will need to record the value of assets as at 1 July 2027. Income support recipients will be exempt from the 30% tax so there is an additional bonus to qualify for a part pension or other forms of income support. Small business CGT concessions will also continue unchanged. | ||||||||||||||||||||||

2. Taxing of Family Trust Distributions Effective: 1 July 2028 | A minimum tax rate of 30% will apply to distributions from a discretionary trust, with some exemptions. The tax will be paid by the trustee. Beneficiaries will still need to declare the income in their tax returns, but beneficiaries, other than corporate beneficiaries, will receive non-refundable credits for the tax payable by the trustee, which can be used to offset current year income tax liabilities. Rollover relief will be provided for three years from 1 July 2027 to assist small businesses and others that wish to restructure into companies or fixed trusts. The new rules will not apply to primary production income and other trusts such as fixed trusts, income from assets of existing discretionary testamentary trusts, deceased estates and superannuation funds. The Government will consult with stakeholders on key details of this policy including the mechanism for collecting the minimum tax on trusts, how trustees use excess franking credits and details of rollover relief for restructuring. | Consider the ongoing viability of existing family trusts. Although non-refundable, the credits may reduce the tax otherwise payable on other income. Consider holding assets in individual or joint names. Fixed trusts may provide an alternative vehicle to access the benefits of succession planning and asset protection. Consider the ongoing viability of existing and future testamentary trusts. | ||||||||||||||||||||||

3. Restrictions on Negative Gearing for Residential Property Effective: 1 July 2027 | Negative gearing on residential property will be restricted to new builds that genuinely add to housing supply. Existing arrangements will remain unchanged for all properties held as at Budget night. Investors who buy established housing after Budget night will still be able to deduct losses against residential property income. They will be able to carry forward unused losses to future years but won’t be able to deduct them against other income like wages. | Gearing (and potentially negatively gearing) in other assets such as shares or commercial property is not restricted. The use of negative gearing as a wealth creation tool will significantly diminish. The demand for and hence the price paid for new builds may obtain a boost. The demand for and hence the price paid for existing builds may be stunted to some degree. | ||||||||||||||||||||||

4. Personal Income Tax Effective: 1 July 2026 | This table sets out the current personal income tax rates together with the new tax rates from 1 July 2026. These changes were announced in the March 2025 Federal Budget and have since been legislated.

¹Reducing to 14% in 2027/28. | A modest reduction in the lowest marginal tax rate from 16% to 15% in 2026/27 and to 14% in 2027/28, will bring the following savings to taxpayers on incomes equal or higher than $45,000:

| ||||||||||||||||||||||

5. Reducing Fringe Benefit Tax (FBT) Exemptions for Electric Vehicles (EVs) Effective: 2026/27 tax year | Reducing the FBT exemption for EVs by transitioning to a permanent 25 per cent FBT discount on eligible EVs over $75,000 from 1 April 2027 and for all eligible EVs from 1 April 2029. Eligible vehicles are those EVs under the luxury car threshold, currently $91,387. | The move to EVs will be driven by interest in renewable energy and a move away from petrol / diesel rather than by tax incentives. | ||||||||||||||||||||||

6. $250 Working Australians Tax Offset (WATO) Effective: 2027/28 tax year | A new tax cut for every working Australian taxpayer through the $250 WATO. | This increases the effective tax-free threshold by nearly $1,800 to $19,985 for workers (or up to $24,985 for workers eligible for the Low-Income Tax Offset). For older Australians who are also eligible for the Seniors and Pensioners Tax Offset, the new effective tax-free threshold including WATO is $38,940 for a single person or $34,726 for a member of a couple. Sole traders will be able to utilise the tax offset. This does not apply to individuals earning just passive income from investments. | ||||||||||||||||||||||

7. $1,000 Instant Tax Deduction Effective: 2026/27 tax year | Allows workers to claim $1,000 of work-related deductions without providing receipts when they lodge their 2026–27 (and future) tax returns. Charitable donations and other non-work related deductions can continue to be claimed on top of the instant tax deduction, as will union or other trade, business or professional association memberships. | This will help workers cut back on paperwork and save them time and money at tax time. Tax savings are expected to average around $200 per person. Eligible taxpayers may wish to submit their 2027 tax return as soon as practicable after the end of the tax year. Expected to apply only to those showing salary or wages in their tax return (and possibly to sole traders). | ||||||||||||||||||||||

8. Other Initiatives |

| |||||||||||||||||||||||

Superannuation | ||||||||||||||||||||||||

1. Taxation of Large Superannuation Balances (previously announced and has since become law). Effective: Effective from the 2026/27 tax year. | The tax on large superannuation balances (Division 296) is legislated to commence 1 July 2026. This applies an additional 15% tax on the taxable income (as adjusted) of the members balance in relation to the excess of their superannuation balance over $3m. The additional 15% tax rises to 30% for the proportion of member balances over $10m. | Affected members should assess their marginal tax rate in super (potentially 30% or 45%) and compare to their marginal tax rate if investments were held in their own name or in a company. Seek advice if affected as this can be complicated. | ||||||||||||||||||||||

2. Other Superannuation Initiatives (including items already announced) |

| |||||||||||||||||||||||

Social Security | ||||||||||||||||||||||||

1. Other Social Security and Aged Care Initiatives |

| |||||||||||||||||||||||

This list is a summary of the May 2026 Federal Budget in so far as it generally affects clients of Allied Wealth. It is not meant to be an exhaustive list of issues and strategies to consider. The information has been sourced from various Government websites. Allied Wealth believes that the information herein is accurate and reliable, but no warranty on accuracy or reliability is given and no responsibility arising in any way for errors or omissions (including responsibility by reason of negligence) is accepted by any member of the company or its representatives. This disclaimer is subject to any contrary provisions of the Competition and Consumer Act. Taxation considerations are based on current laws and their interpretation at the date of preparation of this paper.

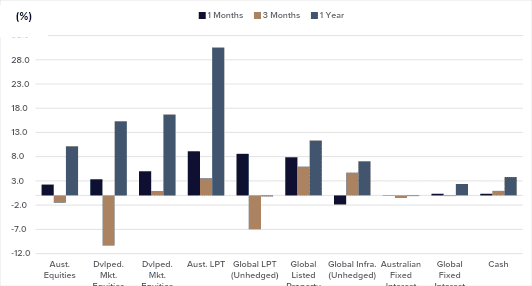

Asset class returns rebounded in April following drawdown in risk assets in March due to the Middle East conflict. Energy costs spiked as the conflict between US and Iran choked off the transport of oil via the Straits of Hormuz.

Source: Allied Wealth, Morningstar.

Coming into Q1 2026, economic growth remained positive while inflation conditions globally (excl. Australia) moderated. These relatively benign conditions were subsequently overshadowed by a sharp energy price shock and supply-side disruptions from the escalating conflict.

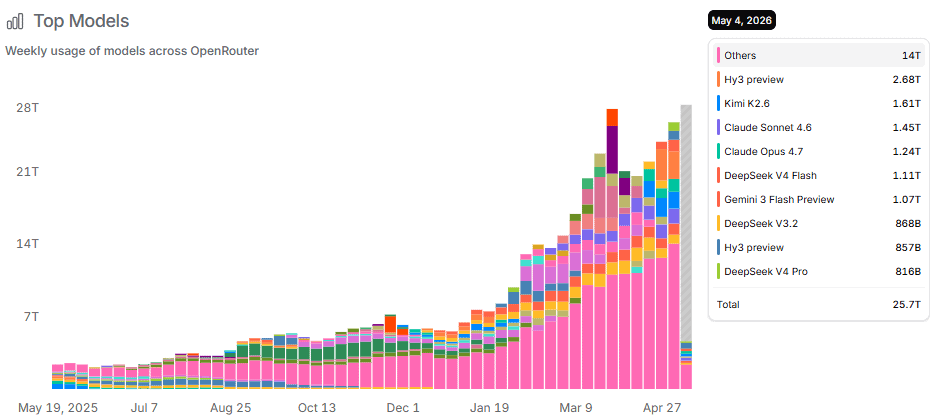

Since February 2026, investor sentiment toward technology and AI-related sectors has become more cautious, reflecting increased scrutiny of long-term earnings growth assumptions. We view the return of valuation discipline as constructive for the sector. At the same time, evidence of enterprise-level AI adoption is emerging (see AI-model usage in Figure 2), alongside development of real-world use cases at the software layer. This trend is corroborated by material revenue growth noted among leading AI model providers, including Anthropic.

Source: OpenRouter

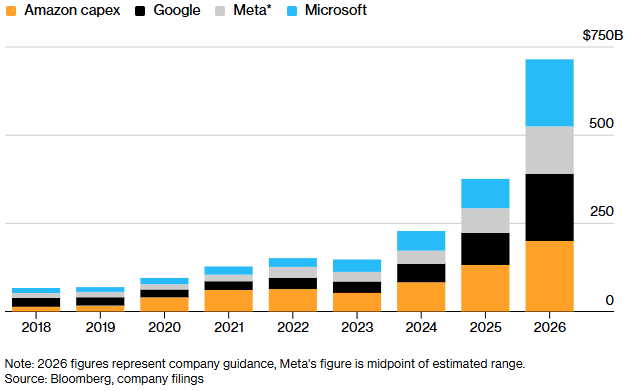

Our assessment of this thematic suggests that, over the long term, corporations are likely to be the primary beneficiaries of AI adoption, with gains coming at the expense of consumers and segments of the workforce. Early data indicate that margin expansion is being driven by a combination of productivity gains and labour force rationalisation. While we do not expect immediate disruption to employment, we anticipate that the impact will emerge through structurally lower junior-level hiring, with potential implications for youth unemployment.

In contrast, elevated capital expenditure on data centres and energy infrastructure is expected to provide ongoing support to economic growth (Refer Capex by Hyperscalars in Figure 3 below).

In the Middle East, more than two months have passed since the conflict began. At the time of writing, an open-ended ceasefire remains in place with markets expecting a gradual re-opening of the Straits of Hormuz. It remains too early to tell at this point and the experience over the last two months remind us to expect the unexpected.

Despite the persistent tensions, we believe there are compelling incentives for all parties to pursue a negotiated resolution. For Iran, such an outcome would enable the continuation of oil exports and may facilitate broader economic benefits through potential sanctions relief. For the US, prolonged conflict and elevated energy prices carry growing political costs, particularly ahead of the mid-term elections scheduled for November 2026. Whilst the balance of incentives favours de-escalation, the timing remains uncertain. Until greater clarity emerges, equity and energy markets are likely to remain highly sensitive to regional developments.

Unlike many advanced economies, Australia experienced a re-acceleration in inflation even before the onset of the US-Iran conflict. This dynamic has been exacerbated by Australia’s structural dependence on Asian oil refineries, which themselves rely heavily on crude oil shipments from the Middle East, leaving domestic prices more exposed to external energy supply shocks.

In response, the Reserve Bank of Australia has tightened monetary policy aggressively, raising interest rates three times so far in 2026, with financial markets currently pricing in a further rise in August. Whilst these developments are likely to fuel a near-term lift in headline inflation, our medium-to-longer-term outlook remains consistent with a gradual moderation in price pressures.

This inflation episode differs materially from the post-COVID surge Australia experienced in 2022 and 2023. That period was characterised by unprecedented fiscal stimulus, severe supply-chain disruptions, and historically tight labour markets, which together resulted in persistent inflationary pressures. By contrast, current labour market conditions are materially weaker, with slower wage growth and easing employment momentum. These conditions reduce the risk that short-term price shocks translate into sustained inflationary pressures. Whilst inflation volatility is likely to remain elevated in the near term, the underlying macroeconomic backdrop suggests a lower probability of a prolonged inflation spiral.

Short-term economic growth is likely constrained by the energy-driven supply-side shock. However, we believe the structural drivers of long-term growth remain intact underpinned by sustained capital expenditure in AI and energy infrastructure. Additionally, we have observed clear evidence of enterprise-level AI adoption, supported by tangible use cases at the software layer. Our analysis suggests that corporates are the primary beneficiaries, with improvements in profit margins driven by productivity gains and workforce rationalisation, although this thematic is expected to unfold gradually over an extended period.

Following the recent market drawdown, equity valuations have become more compelling. Whilst short-term market volatility is likely to persist amid geopolitical risks, we believe current valuation levels offer an attractive entry point. Accordingly, we have implemented a modest increase in portfolio risk, expressed through an overweight position in international equities, funded by a corresponding underweight to fixed interest.

The Australian dollar appreciated over the quarter, with foreign exchange valuations now approaching fair value. While the historical overweight to AUD-hedged exposures has contributed positively to returns, we believe the more prudent approach at this juncture is to transition the portfolio to an unhedged AUD position.

| Asset Class | Portfolio Stance | Commentary |

|---|---|---|

| Domestic Equities | Neutral | We maintain a Neutral portfolio stance in Australian equities. The Australian economy remains more exposed to the energy shock compared to its global counterparts. However, valuations at this point are more attractive on a relative basis. Given the competing conditions, we prefer to maintain a Neutral stance. |

| International Equities | Overweight | We have moved to a marginal overweight position in International Equities. Long-term growth drivers remain intact and the recent market sell-off provides a good valuation entry point. Within the asset class, we have selected to remove the exposure to Hedged AUD as foreign exchange valuations are now trading at approximately fair-value. |

| Property and Infrastructure | Neutral | Property and infrastructure as an asset class have remained volatile and reactive to interest rates. Goodman Group represents almost 40% of the Australian listed property index. |

| Fixed Interest | Underweight | We have moved to an underweight portfolio stance. Given the inflation-related market shock, this asset class has experienced volatile trading conditions. The underweight also represents a funding position for International Equities. |

| Cash | Neutral | We have retained a Neutral cash allocation in our portfolios. |

Allied Wealth Investment Committee

Allied Wealth's core principles

You are welcome to pass on this commentary or our contact details to anyone whom you think would benefit from our services.

Disclosure

The information provided in and made available through this document does not constitute financial product advice. The information is of general nature only and does not consider your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice.

We recommend that you obtain your own professional advice before making any decision in relation to your particular requirements or circumstances.

Allied Wealth Pty Ltd is a Corporate Authorised Representative of Allied Advice Pty Ltd for financial planning services. AFS Licence No. 528160

Every February and August, most Australian listed companies reveal their profit results and guide how they expect their business to perform in the upcoming year. While we regularly meet with companies between reporting periods to gauge their business performance, the reporting season offers investors a detailed, externally audited view of the company's financials.

The recently concluded February 2026 company reporting period highlighted how volatile earnings season can be when the market is at all-time highs, with investors nervous about rising geopolitical tensions. The dominant themes of the February reporting season have been that Australian consumers continue to spend despite rate hikes, that Trump's tariffs have had a negligible impact, that bank profits are high, and that most companies presented a solid economic outlook.

Overall, February 2026 showed that Australian corporates are in better health than expected, with profits showing minimal negative impact from geopolitical events such as Trump's ever-changing trade policies. This saw the ASX 200 hit an all-time high, led by the large miners and banks. This week's piece looks at the key themes from the reporting season that fared last week, the best and worst results and how the Allied Wealth Direct Equities Portfolio performed over the month.

This February reporting season continued the volatility we saw in 2025. The average intraday share price move was 8% among the stocks that reported, with 12 large-cap companies recording share price moves of more than 10% on results day. This is very unusual, as the fortunes of the largest Australian companies rarely change significantly in the short term, with no company revealing a profit result warranting changes of billions to its valuation. Cochlear's first-half profit was $7M below expectations and only 10% growth for 2026; however, this saw $3.5 billion wiped off the hearing device company's market capitalisation on the day they released their results.

More confusing was the market reaction to JB Hi-Fi's result, which initially rose 4%, then fell 4% (a swing of 8%) before finishing up 7.5% at 4 pm, moves that saw us, as shareholders, tearing our hair out. Apparently, the AI bots had trouble interpreting the profit results from the electrical goods retailer. We see this as the result of the increasing influence of momentum trading driven by computerised programs immediately after company results are released.

Retailing has been a mixed bag over the last 6-12 months, with consumers becoming more value-conscious, making discount and promotional periods even more important for sales growth. Discount retailer JB Hi-Fi saw sales increase by 7% over the period, driven by higher sales during Black Friday and Boxing Day. The opposite could be said of Domino's Pizza, which saw Australian sales fall by 8% as it stepped away from heavy discounts and promotional periods.

Wesfarmers similarly announced that it is repositioning how Officeworks approaches the market and its value proposition for customers. Officeworks is currently undergoing a transformation program to move to a lower-cost operating model, which will support lower product pricing and enable it to compete more effectively during promotional periods. Wesfarmers' other key retail divisions, Bunnings and Kmart, have been the lowest-cost operators in their respective fields of hardware and discount department store retail for some time, which has enabled them to continue taking market share and increasing profits. The message for investors is to invest in the lowest-cost operator.

Domestically focused companies benefited from Australia's comparatively resilient Economy, supported by a strong labour market and steady population growth. Without exposure to slowing international economies, geopolitics, and foreign exchange swings, these domestic companies were able to deliver resilient, stable earnings.

Since the start of the year, we have seen an increase in negative international geopolitical news, including new tariffs, actual wars, presidential captures, and plans to take over Greenland. All of these have caused negative moves on the ASX but ultimately had minimal impact on profits.

Higher copper prices played a major role in lifting earnings for major ASX 200 miners, with BHP delivering one of the standout results of the season. The company reported that copper earnings surpassed iron ore for the first time in its history, a shift directly linked to the strong rally in copper prices driven by electrification demand and tight global supply. This surge helped BHP post a stronger-than-expected half-year result, contributing to a broader wave of profit upgrades across the resources sector. Other diversified miners such as South32 also benefited from the uplift in base and precious metal prices, reinforcing copper's growing importance as a profit engine.

Gold producers also enjoyed a stronger earnings backdrop, driven by rising gold prices, which supported safe-haven flows amid global volatility. Northern Star is one of the companies benefiting from the commodity-price tailwind, with higher realised gold prices helping lift margins and earnings. This strength in gold helped miners outperform the broader ASX 200 on several trading days, even as most other sectors were under pressure. The combination of elevated gold prices and surprisingly resilient production volumes positioned gold miners in a strong position heading into 2026.

Commonwealth Bank provides a good look through the Economy during reporting season, with Australia's largest bank holding over 17 million customer accounts. Consequently, the big banks' financial results and accompanying 174-page reporting suite give investors an insight into the health of the various sectors of the Economy. CBA showed minimal bad debts and rising dividends, but also that higher interest rates had differing impacts across their customer base. Discretionary spending decreased on average over the last year for customers aged 35+, while customers aged 35 and below increased spending from a low base last year.

The CBA result highlighted the underlying resilience of the Australian Economy despite stronger economic activity, inflation, and labour markets. The bank did highlight that stubbornly high inflation will likely see the cash rate increased twice over the year to 4.1%. These increases in the cash rate are unlikely to trigger a dramatic spike in bad debt, with most mortgage holders having rebuilt their savings buffer over the last 18 months.

Over the month, Lynas Rare Earth, Iluka Resources, NRW Holdings, PLS Group, and Tabcorp delivered the best results. These companies benefited from higher commodity prices and operational efficiencies.

Looking on the negative side of the ledger, Temple and Webster, Web Travel, Pro Medicus, Data #3, and ZIP reported results that were poorly received by the markets. The common themes amongst this group were underdelivering on growth when trading on a high P/E, and the prospect that AI could replicate their offerings for much lower cost.

Before the February 2026 reporting season, everyone understood that copper was becoming a more central part of BHP's earnings. Few expected copper to account for 51% of BHP's earnings. This increase in copper earnings was driven by a 32% increase in the copper price over the first half of 2025. This increase saw profits rise 34% to $12.3 billion, with the dividend rising 44% to US$0.73 per share. Even more unexpected was the entry into a long-term streaming agreement with Wheaton, in which Wheaton receives BHP's share of silver production from Antamina copper mine in Peru for US$4.3 billion. Unusually, the result of the season comes from a large company.

When a company reports a result, one of the first things we look at is the dividend paid, as this is the best indicator of a company's actual health. A company's board is unlikely to raise dividends if business conditions are worsening. Also, earnings per share can be restated later due to "accounting opinions" or financial shenanigans from the company's finance team. However, once dividends are paid into bank accounts, they cannot be reclaimed.

Source: Allied Wealth.

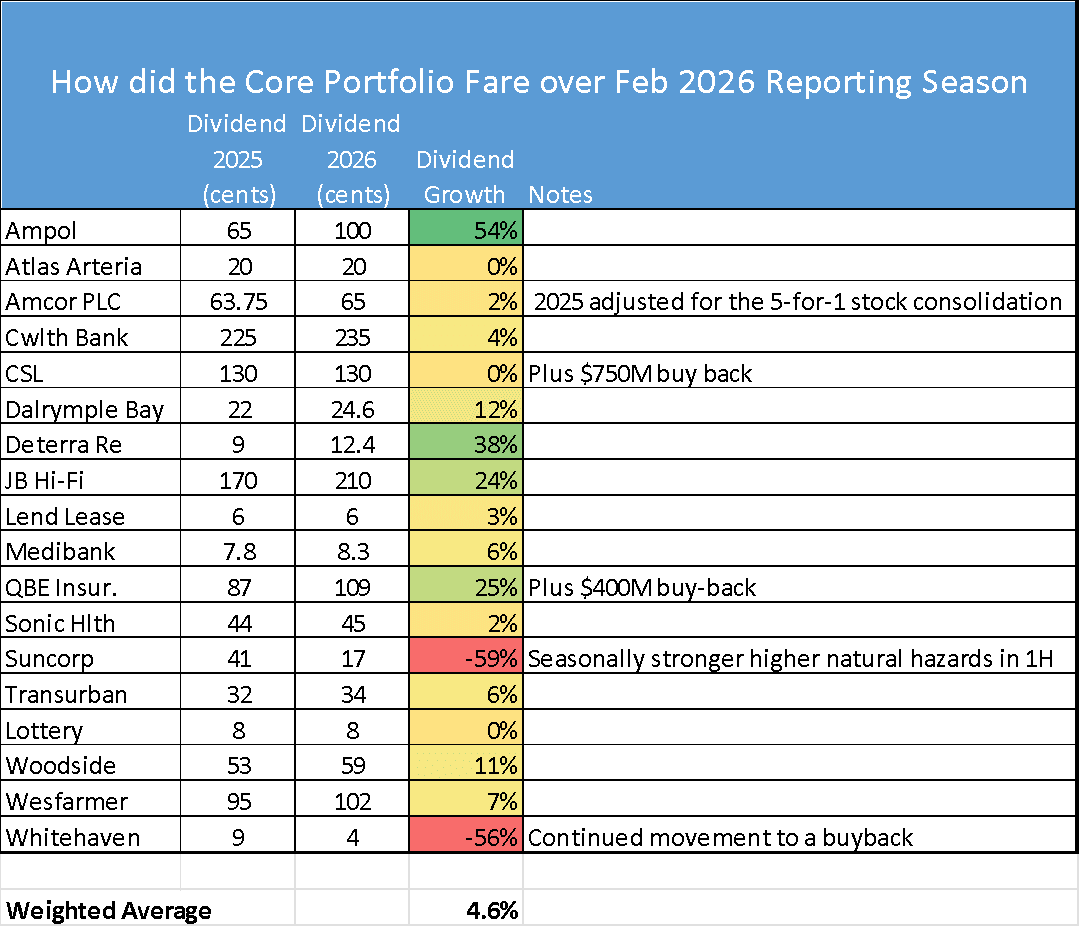

Using a weighted average across the Allied Wealth Direct Equities Portfolio, our investors' dividends will be +5% higher than in the previous period in 2025 and significantly ahead of inflation. We see that dividends are a better measure of a company's financial health than earnings per share. In the short term, the market is a voting machine that rewards popular companies; in the long term, it is a weighing machine that rewards companies that consistently pay increasing dividends to shareholders.

Source: Allied Wealth, Bloomberg (Data as at 10th March 2026 close)

The ongoing escalation of violence in the Middle East remains a material risk that markets find difficult to quantify. Our analysis indicates that investors’ primary concern centres on rising oil prices and the flow-through impact on inflation, and interest rates. This dynamic mirrors what was observed at the onset of the Russia-Ukraine conflict.

In equity markets, sentiment towards Technology and AI-related sectors has become more measured. Investors are reassessing valuations and recalibrating long-term earnings assumptions, which has contributed to heightened volatility across these segments.

Our medium-term outlook remains Neutral. However, equity valuations have become more attractive following the recent market drawdown. While near-term forecasting is complicated by geopolitical risks, we expect steady economic growth over the medium-term supported by ongoing capital expenditure in digital and energy infrastructure. Where appropriate the current environment provides an opportunity to rebalance portfolios back to targets, selectively increasing risk where appropriate.

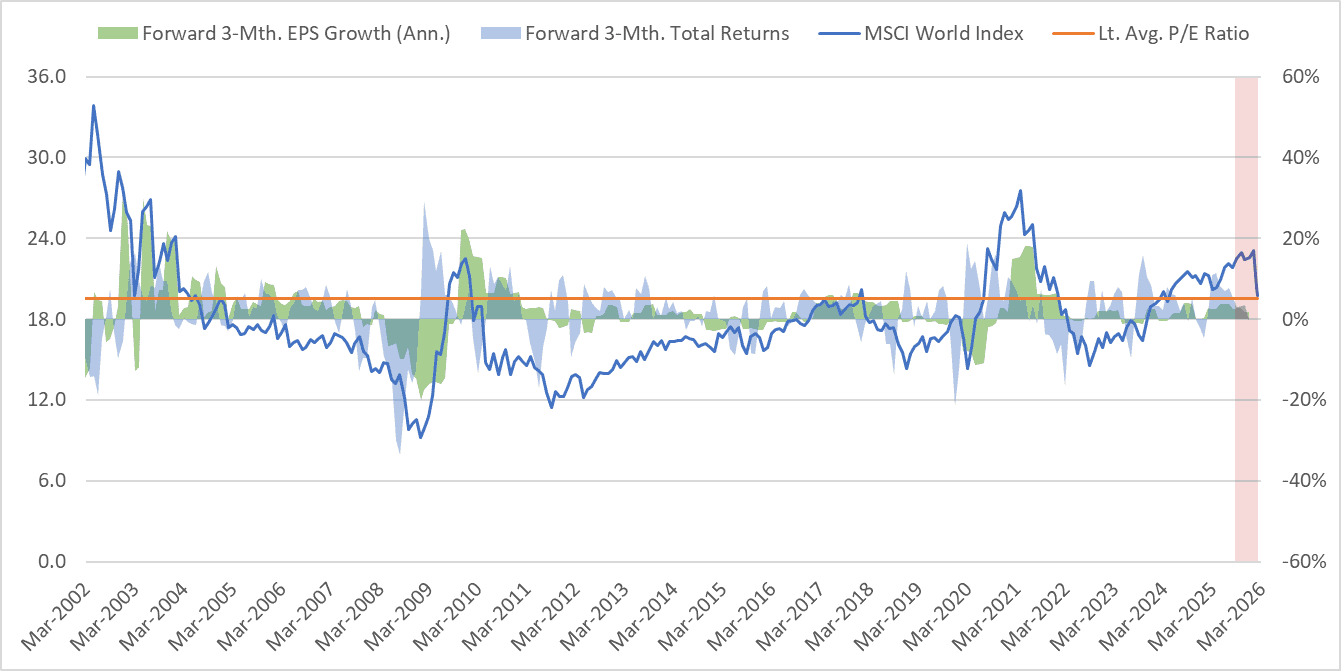

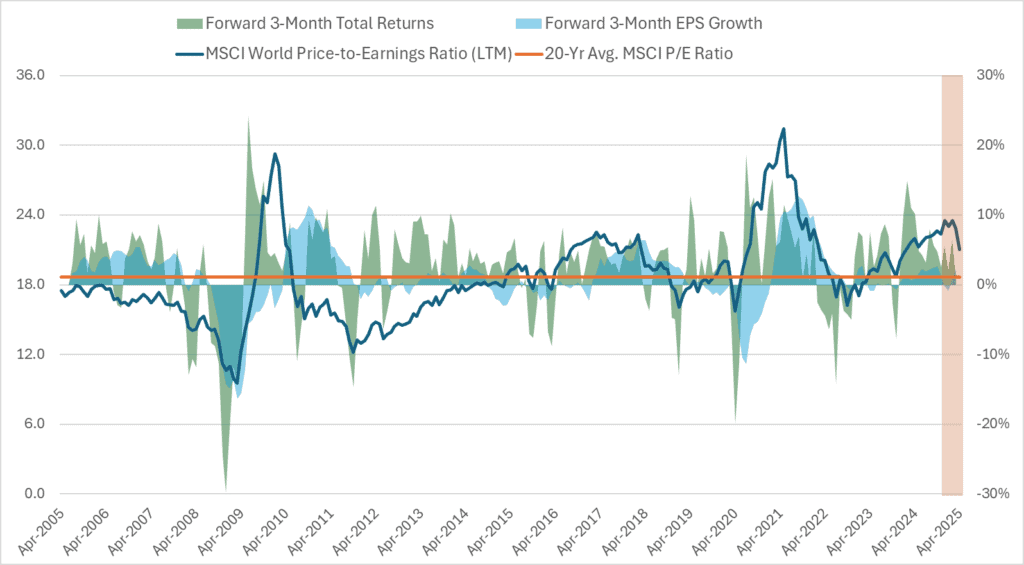

As communicated previously, we see a price-to-earnings entry point around 18x as attractive from a long-term valuation perspective. With global equity markets currently trading near 19.7x, we are closely monitoring market conditions for alignment with our preferred valuation levels; with consideration given to any structural shifts in fundamentals.

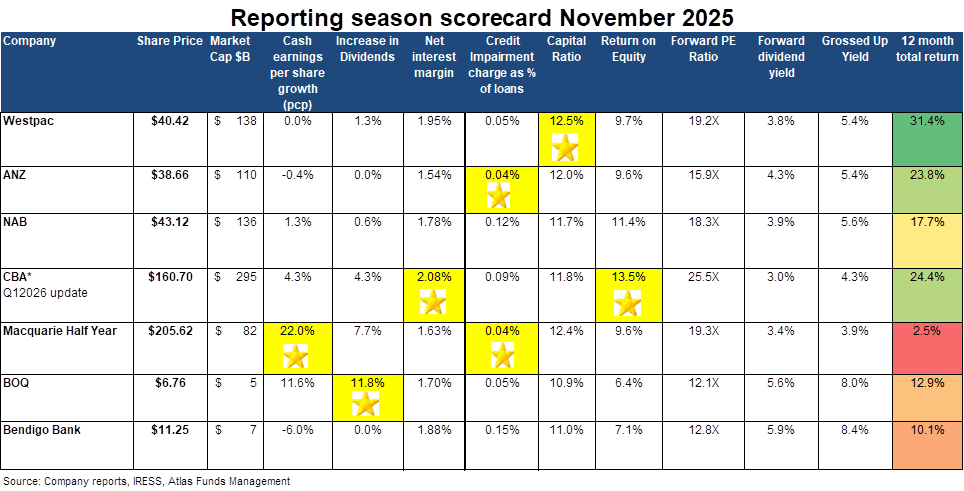

Unlike the past few bank reporting seasons, there was little trepidation from investors going into the November 2025 bank reporting season. The last few bank reporting seasons have been very consistent, with a similar story of high margins, solid loan growth, strong capital, and minimal bad debts. An excellent position for investors with a large weighting to the banks but infuriating for professional fund managers who sold down their bank exposures in early 2024 due to concerns about recession, rising bad debts, and valuation concerns, particularly in the case of the Commonwealth Bank.

In this piece, we look at the major themes played out over the November 2025 bank reporting season. Even for investors that don't own the banks, looking closely at their results provides a window into the financial health of Australia. Overall, we were happy with the banks held in the Allied Portfolio.

The banks, including Macquarie, currently make up 27% of the ASX and is the largest sector on the ASX, significantly higher than miners at 18%. The sector has been the one of the better performing sectors on the ASX in 2025 +14%, ahead of the ASX 200 +9%, though the lead has been pared back since July due to the fall in CBA off -19% since the start of July.

Bad debts remained low throughout 2025, with all banks reporting extremely low loan losses. ANZ and Macquarie reported the lowest bad debts at 0.04% of gross loans, reflecting the continued discipline of banks in not writing loans at any cost. Across the rest of the banks, none reported bad debts exceeding 0.15% of gross loans.

The level of loan losses is important for investors, as high loan losses reduce profits and, consequently, lower dividends due to the resulting lower bank capital base. This reporting season has seen low bad debts translated into better-than-expected profits and, thus, higher dividends.

Bad debts remained low in 2025, with all banks reporting negligible loan losses; Westpac, Macquarie and ANZ reported the lowest level, with loan losses of 0.04%. To put this in context, after the 1992 recession, bank loan losses have averaged around 0.30% of outstanding loans, and banks price loans assuming losses of this magnitude. Similarly, sell-side analysts issue share price targets on the banks, assuming a reversion in losses at this level. We believe the loans to developers, property syndicates and troubled industrial companies that are impaired now sit with non-bank lenders and private debt funds rather than the big four banks.

In the November 2025 bank reporting season, the banks announced smaller increases in dividends than we have seen over the last few years, with the average dividend increase across the big banks being 1%. Macquarie Bank had the largest dividend increase of 8%, with ANZ at the other end, holding the dividend the same as they did last year.

Interestingly ANZ not cutting the dividend was probably one of the bigger pieces of news in the reporting season, with the consensus view being that ANZ’s new CEO would adopt the traditional playbook of an incoming CEO – blame previous management for errors, increase provisions and cut the dividend to “preserve capital” – thus allowing the CEO to look good in future years as the provisions are written back (boosting reported profits) and the dividend increased.

Pleasingly ANZ’s CEO announced a cost-cutting exercise and kept the dividend saying that the bank was in good shape, this saw the share price bounce 10%.

Franking account balances in the banks remain very strong with CBA sitting at $2B in excess credits, Westpac is still the leader with $3.7B as a consequence of not paying an interim dividend in 2020 and being slower to pay full dividends coming out of CV-19. Bank investors can look forward to a solid stream of franked dividends for the foreseeable future. Indeed, the franking balances in the banks are likely to build further in coming years with the retirement of hybrids, many banks had used hybrids as a means to stream out excess franking credits.

In 2025, the Australian banks are all very well capitalised and have seen their capital build. This enables banks to return capital to shareholders through on-market buybacks and increased dividend payments. While the banks have not been actively buying back their shares recently, the ongoing buybacks serve as a sort of floor in the share price, with the banks stepping back into the market to purchase shares when the share price falls below a certain threshold. Indeed, CBA's $1 billion market buyback last bought back a share on November 15, 2024, at $151 per share.

Overall, we are happy with the financial results from the banks owned by the Allied Australian Equity Portfolio in November. Westpac, ANZ and Macquarie either maintained or increased their dividends, with the market expecting ANZ's new CEO to usher in a rebasing of the dividend lower.

All banks demonstrated solid net interest margins, low non-performing loans, and effective cost control. In 2026, the banks will all have cleaner loan books, more consistent earnings and a greater margin of safety than they have had in the past.

In a turbulent world with weekly changes in trade policies, Australia's major banks are likely to continue positively surprising the market, operating in a small oligopolistic market, sheltered from both new competition and global storms. Allied Wealth has been more optimistic towards the banks than most over the past few years, which has been positive for our investors. However, given current valuations and portfolio construction constraints, we are likely to reduce our holdings and would need CBA to fall more before we bought back the stock we sold earlier on in 2025.

Asset class returns ended the quarter broadly positive. Despite bouts of volatility, risk assets have continued to trend higher. We remain concerned about the persistent rise in asset values given observed weakness in some underlying economic data. That said, monetary policy considerations may continue to support price appreciation even in the absence of improving fundamentals.

Source: Allied Wealth, Morningstar.

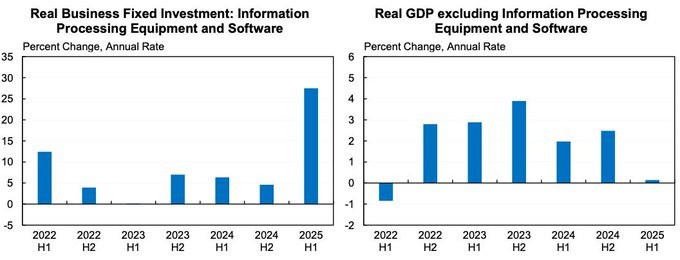

Headline real GDP growth across developed markets remains positive, though the drivers are narrow. A significant portion of growth is attributable to AI-related capital expenditure across hardware, software, and data centre infrastructure. Excluding these effects, growth appears anaemic.

Source: Jason Furman

Whilst AI-driven investment is creating near-term activity in construction and engineering, the long-term productivity gains remain untested. Early signs suggest AI may be more useful for employment consolidation rather than revenue expansion, with technologies such as SoraAI and Copilot reshaping labour demand across creative and professional sectors.

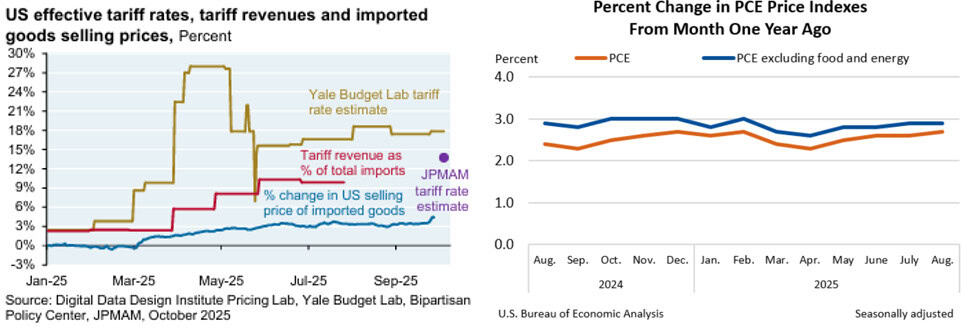

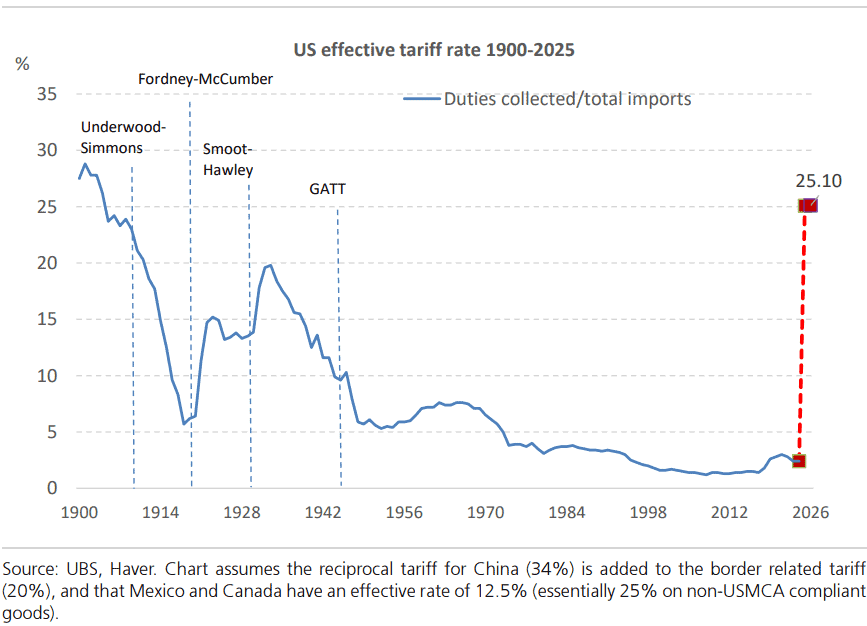

So far in 2025, the U.S. federal government has collected a record $195 billion in customs duties under the expanded tariff regime. More recently, the U.S. Trade Court ruled that the majority of tariffs enacted by President Trump under the International Emergency Economic Powers Act (IEEPA) are illegal—a decision upheld by a federal appeals court and now awaiting Supreme Court review.

Whilst tariff revenues have risen, the inflationary impact has been muted, with limited pass-through to consumer prices observed. So far, the U.S. Core PCE index (the Federal Reserve’s preferred inflation gauge) has remained stable over recent quarters.

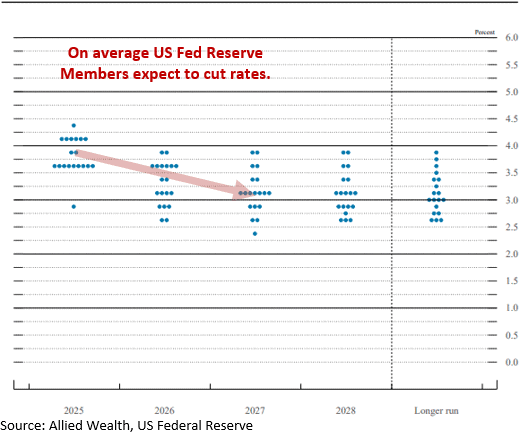

The combination of weaker underlying growth and stable inflation provides a case for further policy rate cuts by central banks. This outlook is reflected in the trajectory of rate cuts signalled by members of the U.S. Federal Reserve.

We remain cautious on equity market valuations, which continue to look elevated. Recent performance of International Equities has been disproportionately driven by unprofitable technology companies with limited fundamental justification, yet these segments have contributed materially to index-level returns.

This concentration of gains in speculative areas highlights the fragility of the rally, with sentiment rather than earnings strength dictating market outcomes. Nonetheless, a falling rate environment supporting lower financing costs and improved liquidity remains a powerful tailwind. This dynamic may continue to drive equity markets higher despite richly priced fundamentals.

Against this backdrop, market timing remains extremely challenging. In line with the current outlook, the Investment Committee has elected to retain a Neutral portfolio stance, while maintaining our overweight to hedged international equities relative to unhedged exposures. Looking to the long term, we are actively monitoring equity markets with a view to increasing allocations should valuations become more compelling.

| Asset Class | Portfolio Stance | Commentary |

|---|---|---|

| Domestic Equities | Neutral | We maintain a Neutral portfolio stance in Australian equities. Increasing stock concentration is skewing analysis for the asset class. Earnings have continued to remain resilient, but valuations are expensive. |

| International Equities | Neutral | We have maintained a Neutral position in International Equities; but within the asset class, have selected to maintain the marginal overweight to hedged International Equities (relative to unhedged). |

| Property and Infrastructure | Neutral | Property and infrastructure as an asset class have remained volatile and reactive to interest rates. |

| Fixed Interest | Neutral | We maintain a Neutral portfolio stance. Geopolitical uncertainty is contributing to some volatility in this asset class, but rates are expected to still provide downside protection in an economic downturn. In balancing both the upside and downside considerations, maintaining a neutral stance remains the prudent course of action. |

| Cash | Neutral | We have retained a Neutral cash allocation in our portfolios for buying opportunities should equity valuations reach attractive levels. |

Allied Wealth Investment Committee

Allied Wealth's core principles

You are welcome to pass on this commentary or our contact details to anyone whom you think would benefit from our services.

Disclosure

The information provided in and made available through this document does not constitute financial product advice. The information is of general nature only and does not consider your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice.

We recommend that you obtain your own professional advice before making any decision in relation to your particular requirements or circumstances.

Allied Wealth Pty Ltd is a Corporate Authorised Representative of Allied Advice Pty Ltd for financial planning services. AFS Licence No. 528160

Asset class returns ended the quarter broadly positive. Incoming economic data was mixed. Despite some negative economic data prints equity, credit and rate markets have trended positive.

Source: Allied Wealth, Morningstar.

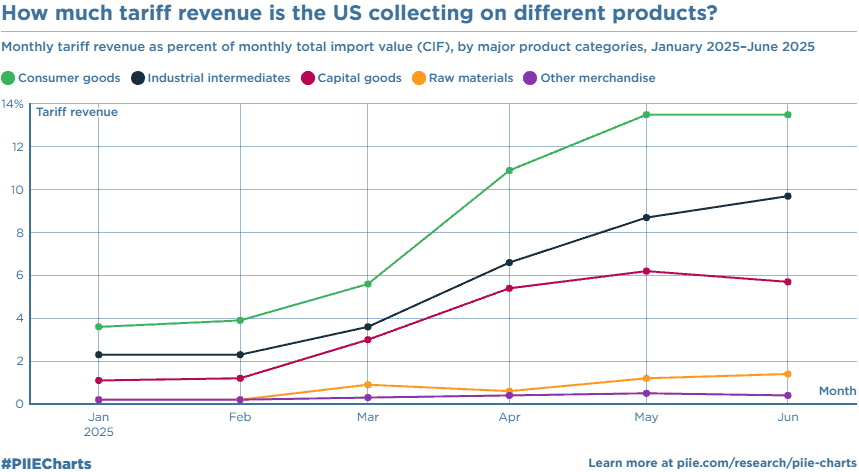

Since his inauguration earlier this year, President Trump has weaponised US trade policy and created both corporate and economic uncertainty for US consumers and global trading partners. Despite claims that multiple bilateral trade agreements have been reached, implementable details have been lacking. We are not convinced that there will be trade stability given his volatile nature and penchant for walking back on previous agreements. What is certain today are tariff are here to stay. Tariff collections have started, and at current levels is estimated to bring in approximately USD 330 Billion p.a. We have begun to see a slight uptick in US core inflation and expect this to trend upwards as the year progresses. Surveys conducted with US importers suggests that companies are planning to pass on 70% of tariffs in 2025, increasing it to 100% in 2026 and onwards.

Source: Peterson Institute

Reported corporate earning in Q2 2025 demonstrate some level of earnings resilience but the impact of companies front-running tariffs through excess importing should not be underestimated. Much like the tariff pass-through we think the consumer pain will likely only appear in the data prints sometime in the fourth quarter. Indeed, early labour market indicator such as the initial jobless claims have marginally increased in August.

Source: Trading Economics

In addition to upending trade policy, Trump has been trying to influence the outcome of monetary policy suggesting in press conferences that US policy rates should be lowered to 1%. (For context, US policy rates are currently 4.33%). Should he be successful, this would mean an end to the independence of the US Federal Reserve which have been an independent and apolitical institution since 1951.

Australia is unlikely to be immune to the impact of policy changes, but given our geographic location and economic linkages, we are likely to experience the second-order effects. At the time of writing, Australia’s GDP growth was 1.4%; with inflation hovering around 2.1%. Despite the RBA’s reticence, we think the central bank will be forced to cut rates in the coming quarter, given the weakening observed in the labour market. We expect our growth trajectory to be affected by a slowing Chinese economy.

US trade and monetary policy are key economic uncertainties. Despite headwinds, we expect corporates to continue to muddle through this environment. Tariffs will likely remain a feature of market going forward, with only the level changing.

Market timing in this environment remains extremely challenging. In-line with the current outlook, the Investment Committee has elected to retain the Neutral portfolio stance, while maintaining our overweight to hedged international equities relative to unhedged. Focusing on the long-term, we are actively monitoring equity markets with a view of increasing our allocation should market valuation become compelling.

| Asset Class | Portfolio Stance | Commentary |

|---|---|---|

| Domestic Equities | Neutral | We maintain a Neutral portfolio stance in Australian equities. Increasing stock concentration is skewing analysis for the asset class. Earnings have continued to remain resilient, but valuations are expensive. |

| International Equities | Neutral | We have maintained a Neutral position in International Equities; but within the asset class, have selected to maintain the marginal overweight to hedged International Equities (relative to unhedged). |

| Property and Infrastructure | Neutral | Property and infrastructure as an asset class have remained volatile and reactive to interest rates. Goodman Group represents almost 40% of the Australian listed property index. |

| Fixed Interest | Neutral | We maintain a Neutral portfolio stance. The evolution of trade policy, potential for economic recession and inflation have a wide set of implications for the asset class. In balancing both the upside and downside maintaining a neutral stance remains the prudent course of action. |

| Cash | Neutral | We have retained a Neutral cash allocation in our portfolios for buying opportunities should equity valuations reach attractive levels. |

Allied Wealth Investment Committee

Allied Wealth's core principles

You are welcome to pass on this commentary or our contact details to anyone whom you think would benefit from our services.

Disclosure

The information provided in and made available through this document does not constitute financial product advice. The information is of general nature only and does not consider your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice.

We recommend that you obtain your own professional advice before making any decision in relation to your particular requirements or circumstances.

Allied Wealth Pty Ltd is a Corporate Authorised Representative of Allied Advice Pty Ltd for financial planning services. AFS Licence No. 528160

At the time of writing (April 5), equity markets have fallen 12% since the beginning of March 2025. The most significant market drawdowns experienced on the 3rd and 4th of April coincided with:

Cumulative tariffs implemented to date represent a reversal of the global trade progression over the last 100 years. Unlike 100 years ago, industrial manufacturing today is more sophisticated and interconnected than ever before. For instance, a car considered “US-made” today still relies on more than 40% non-US manufactured parts.

The magnitude of Trump’s “Liberation Day” tariffs has been far more aggressive than markets anticipated, with retaliatory tariffs by other nations still to come. Negotiations with Trump and his team have proven inconsistent at best, with the US administration abandoning its commitments in a matter of days. This persistent uncertainty in trade policy will continue to weigh on market sentiment.

You may have read multiple articles highlighting the risk of stagflation (persistently high inflation with high unemployment and low growth). We think of this risk as a tail-risk and would assign a low probability of stagflation at this time. Based on the anecdotal reaction by businesses to the tariffs, we think an economic recession over the short to medium term is more likely as businesses delay capital expenditure decisions, reduce their labour force and pass on costs to consumers – all of which will lead to a pullback in consumption and spending. The depth of the economic recession is uncertain and will be highly predicated on how the current situation evolves.

Over multiple client newsletters, we have consistently reiterated the view that markets continue to trade above fundamentals. However, the drawdown experienced to date (refer to orange bar in Figure 2) has moved International Equity valuations closer to an attractive entry point of around 18x. Should extensive drawdowns drive valuations to this desired level, we will review and assess buying opportunities.

Source: Bloomberg, Allied Wealth

While we expect a wide dispersion of outcomes over the short-term, we maintain a more bullish view over the longer-term. As noted in our previous commentary, pain for the consumer does not necessarily equate to a dire outcome for large multi-national corporations (but the adjustment will, of course, hurt!).

Much like the COVID-19 period and the interest rate rise of 2022, large corporates have maintained and grown market share through tough economic conditions at the expense of their smaller counterparts. While we do not think the current environment will be different, we think this adjustment will likely play out over a much more extended time frame. Thus, we are in no rush to increase our equity allocation (i.e., buy the dip) at the current time.

As always, the team at Allied Wealth remains committed to long-term client outcomes. Acknowledging the extremely volatile market conditions, we continue to monitor the geopolitical developments as they change from day to day.

If you have any questions or concerns, please do not hesitate to contact us.

You are welcome to pass on this commentary or our contact details to anyone whom you think would benefit from our services.

The information provided in and made available through this document does not constitute financial product advice. The information is of general nature only and does not consider your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice.

We recommend that you obtain your own professional advice before making any decision in relation to your particular requirements or circumstances.

Allied Wealth Pty Ltd is a Corporate Authorised Representative of Allied Advice Pty Ltd for financial planning services. AFS Licence No. 528160

Every February and August, most Australian listed companies reveal their profit results and guide how they expect their businesses to perform in the upcoming year. While we regularly meet with companies between reporting periods to gauge their business performance, the reporting season offers investors a detailed and externally audited look at the company's financials.

The February 2025 company reporting period that concluded last week highlighted how volatile earnings season can be when the market is at all-time highs. Share price volatility over the month was compounded by Trump's erratic trade policies, imposing and then reversing tariffs dented market confidence. The dominant themes of the February reporting season have been that the consumers continue to hold up, a strong US Dollar, inflation and cost management and a solid economic outlook. This week's piece looks at the key themes from the reporting season that fared last week, the best and worst results and how the Domestic Equities Portfolio performed over the month.

This February reporting season has proven to be more volatile than previous years. The average intraday share price move was 7% from the stocks that reported. Over 20 companies in the ASX 200 saw their share prices move by more than 10% on the reporting day. Small earnings misses saw significant share price moves; similarly, small earnings beats saw large share price movements. For example, A2 Milk posted a small $6 million increase in profits, which saw a $800 million increase in the company's market capitalisation on results day. Conversely, Viva Energy reported a $60 million fall in profits, and $1 billion was wiped off its value on February 25th!

In previous years, we saw prices move similarly to underlying earnings almost one-to-one, but this reporting season saw companies' share prices move over two times earnings revisions. The increased volatility has been attributed to the impact of high-frequency trading funds on setting prices on results day, with long-term holders likely to wait until after meeting management teams or even after the conclusion of reporting season in March before making significant portfolio changes. In February, Woolworths' share price saw a +2.5% gain after releasing their profit results, before falling all afternoon and finishing by -4%. Very frustrating for shareholders of the grocer.

The first dominant theme for the February reporting season was the strength of the domestic consumer. In November 2022, Westpac's economists forecasted a grim year for 2023. The much-feared fixed interest rate cliff is expected to see unemployment rise to 4.5%, an 8% fall in house prices, bad debts spike and retail sales grind to a halt.

Two years on, the February 2025 reporting season showed that consumer demand had not skipped a beat. JB Hi-Fi sales increased by 10% as consumers still demand the best technology and electronic products that will benefit from the AI rollout. Similarly, Kmart and Bunnings Warehouse owner Wesfarmers saw increased sales across its two flagship stores as consumers continued to trade down items, especially to Kmart's Anko brand.

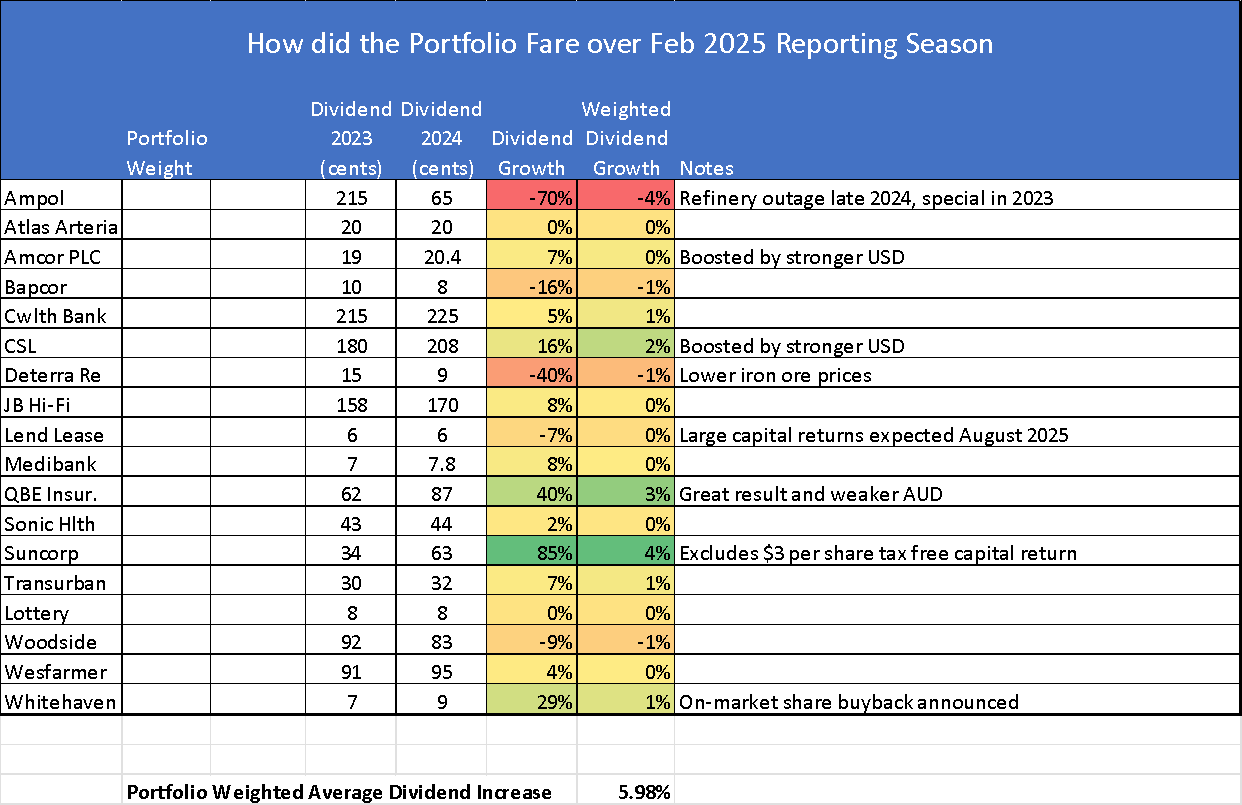

On the negative side, consumers are unwilling to spend on large projects, including building new homes or upgrading bathrooms and hearing implants. This was seen in the results of Reece, which saw profits fall -19%, driven by lower housing starts due to high capital costs in both the United States and Australia. Cochlear surprised the market after reporting that in the USA, cost-of-living pressures have delayed some users' replacement of ageing sound processing technology due to higher out-of-pocket expenses to fund new sound processors.

Since these companies opened their books last August, the Australian Dollar has depreciated against most international currencies, including the US dollar. While this is a negative for those planning ski trips to Aspen or summer trips to Miami, it is a positive for companies that earn profits in the United States or Europe but pay Australian Dollar dividends. The shareholders in these companies saw a free 5% uplift in their dividends from positive currency movements. The clear winners from the weaker Australian Dollar were the commodity miners, who saw their revenue priced in US dollars while their costs largely remained in Australian dollars. Australian companies with a large US presence have also benefitted from this, including Amcor and Brambles, Woodside, CSL, ResMed and QBE Insurance.

Tariffs were frequently posed to management teams in February with a global presence or operations in the USA. However, most Australian companies selling goods or services in the USA should not have a major impact as their manufacturing facilities are generally close to their customers. For example, CSL collects plasma via its network of collection centres scattered throughout the USA, which is then converted into biotherapies at a plant in Illinois. Similarly, Amcor tend to locate their packaging plants close to their US-based customers such as Unilever, Nestle, Novartis and Pepsi, as shipping empty PET drink bottles across borders makes little economic sense.

The main loser from tariffs is likely to be Rio Tino, which will have a 25% tariff on their aluminium from Canada, acquired in their 2007 takeover of Canada's Alcan. Rio mines bauxite in Australia and Brazil, which is then refined into alumina and aluminium in Canada to take advantage of low hydroelectric power costs, and the finished aluminium is sent to customers in the USA.

Breville currently derives half of its sales from the United States, and most of its manufacturing plants are in China, which currently has a 20% tariff on its goods. Explosive manufacturer Orica has a large manufacturing plant in Canada, sourcing cheap natural gas in Alberta to service blasting customers in the USA. The company's Canadian-made ammonia nitrate will now have tariffs placed on it. Conversely, rival Dyno Nobel (Incitec Pivot) may enjoy a sales boost courtesy of Orica from their cheaper explosives produced in Wyoming and Louisiana.

Commonwealth Bank provides a good look through the economy during reporting season, with Australia's largest bank holding over 17 million customer accounts. Consequently, the banks' financial results and accompanying 172-page reporting suite give investors an insight into the health of the various sectors of the economy. CBA showed minimal bad debts and rising dividends but also that higher interest rates had differing impacts across their customer base. While discretionary spending had been cut back along with savings for customers between 20 and 54, older customers above 55 had increased spending and savings.

Insurers continue to have their best results season since the GFC as they enjoy higher premiums, lower claims inflation, lower adverse weather events, and sound investment returns. Suncorp expects gross written premiums to increase by low-mid double digits and margins from inflation moderations. Similarly, QBE expects its gross written premium to increase by mid-single digits over the coming year while benefiting from subsiding cost inflation.

During reporting season, Atlas looks closely at company dividends, particularly the direction of dividends. While our investors appreciate income, the rationale for looking closely at dividends is that increasing dividends is a sign of earnings quality. Our view is that talk and guidance from management can often be cheap, and company CFOs can use accounting tricks to manipulate reported earnings. However, paying out higher dividends tends to signify that "insiders, " company directors, don't see any imminent negative issues.

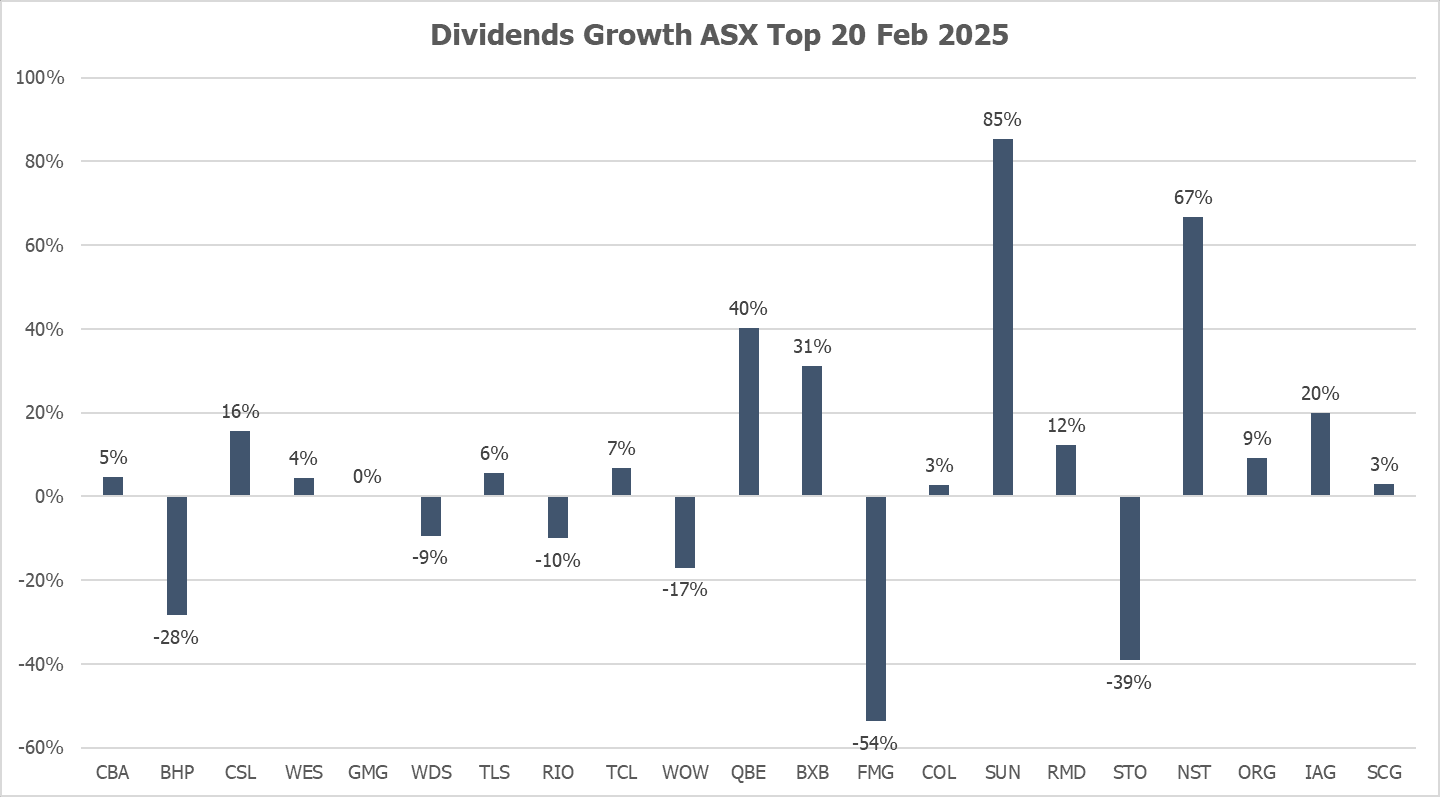

Looking across the top 20 stocks (that reported the other banks having different financial year-ends), the weighted average dividend increase was 0%. The five companies that reduced their dividends, BHP, RIO, Woolworths, Woodside, and Santos, saw weaker commodity pricing.

On the positive side of the ledger, Suncorp, QBE, Northern Star, and Brambles offset the cuts, posting solid increases in cash flows to their shareholders. Across the wider ASX 200, dividends declined by -6% in February.

Over the month, A2 Milk, Computershare, Fletcher Building, Eagers Automotive, and NIB Insurance delivered the best results. Despite the uncertain economic environment, especially around the softening of consumers, these companies were able to grow sales and expand gross margins along with providing optimistic outlooks.

Looking on the negative side of the ledger, Mineral Resources, Viva Energy, Reece, and WiseTech reported poorly received results by the markets. The common themes amongst this group were lower commodity prices (Mineral Resources and Viva Energy) and weaker-than-expected outlooks for higher PE companies (WiseTech and Reece).

Before the February 2025 reporting season, everyone expected that the insurers would have strong financial results, benefitting from slowing claims inflation and higher investment returns on their billion-dollar investment floats. This saw record profits from QBE Insurance and Suncorp, but none better than Medibank Private's results. Medibank continues to grow profits and market share in the Australia Private Health market, which has benefitted from higher premiums, higher uptake of short-stay hospitals and claims inflation slowing. During February, the government approved an average 3.73% increase in health insurance premiums ahead of cost increases. These strong results were achieved while simultaneously returning $1.6 billion to customers through their commitment not to benefit or profit from the pandemic. This is a great outcome that will help Medibank continue growing its market share and benefit the brand and stakeholders.

Overall, we are reasonably pleased with the results from the reporting season for the Atlas Portfolio. In general, the companies in our Portfolio were able to increase earnings and dividends, with some reporting record dividends in a more challenging economic environment.

As a long-term investor focused on delivering income to investors, we look closely at the dividends paid out by our companies and whether they are growing. After every reporting season, Atlas looks to "weigh" the dividends that our investors will receive. While share prices move every second between the hours of 10 am and 4 pm, dictated by changing market emotions, ultimately, the sole reason for buying a share is to access a share of the company's profits paid in the form of dividends.

Indeed, in the February reporting season, we saw several companies, such as NIB and Woolworths, give optimistic outlooks, while cutting dividends. This sends a mixed message to investors, and we would prefer to follow the cash rather than the words! Using a weighted average across the Portfolio, our investor's dividends will be +6% greater than the previous period in 2024, and significantly ahead of the 0% dividend growth seen in the top 20 Australian companies that reported and the -6% decline across the wider ASX.

The Portfolio's dividend increase was also ahead of inflation, which was 2.4% over the period, thus maintaining purchasing power for investors who fund their retirement off income. Based on this measure Atlas are pleased with the results from the February 2025 reporting season.

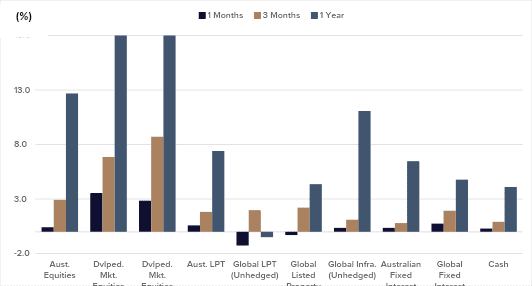

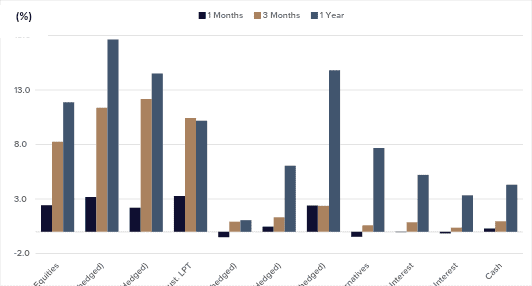

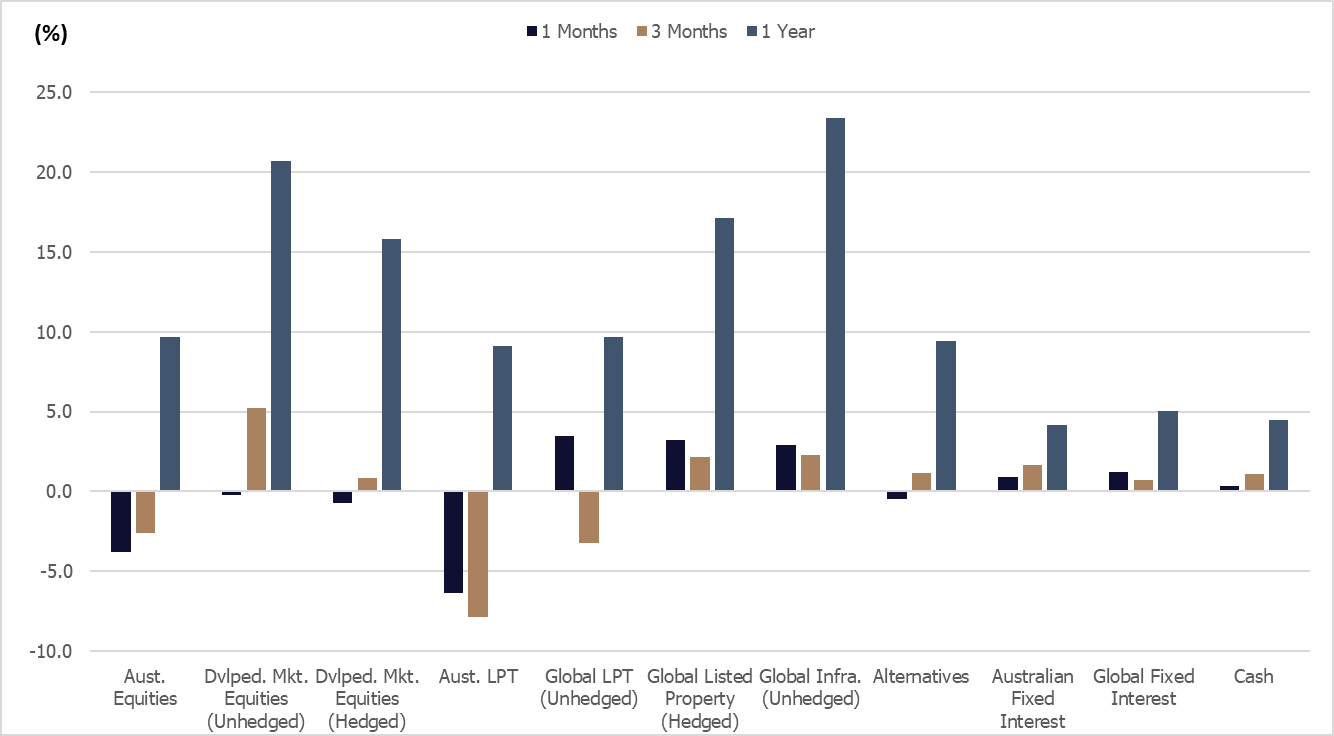

All asset class returns were positive over the 1-year period to February 2024. The Trump presidency and policy uncertainty have resulted in material market volatility over the quarter and negative returns in equities and listed property over the 1-month and 3-month period.

Source: Allied Wealth, Morningstar.

Economically, global and domestic GDP growth while moderate remain positive. Corporate earnings have remained steady but within the listed market, large companies have seen outsized earnings growth compared to smaller counterparts. Despite the Goldilocks (not to hot, not too cold) environment, the largest forces driving markets have been policy uncertainty tied to US trade and fiscal policy. Market reaction has been extreme but in-line with the persistent uncertainty.

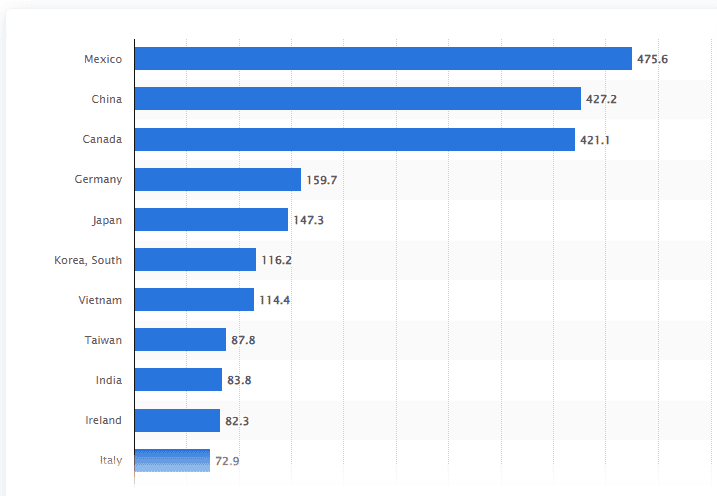

Uncertainty around US trade policy has been the largest driver of market movement over the recent period. Since the inauguration of Donald Trump on the 20th of January the administration has threatened and implemented a 25% trade tariff on Canada and Mexico; with a 20% trade tariff imposed on China. At last count, the Trump presidency has threatened trade tariffs and reversed the decision 6 times in the matter of 7 weeks in office. In our view, trade tariffs are a bad idea and represents an effective tax on the end consumer.

Liberalisation of trade over the last 100 years combined with technological specialisations have resulted in an interconnected global supply chain – e.g. assembly of cars today rely on multiple parts manufactured globally across different countries. Thus, any tariffs affecting the flow of good across borders results in more expensive production costs which is then passed on to consumers by companies looking to maintain their profit margins.

We believe the motivations for tariffs are driven by Trump’s desire to implement a broad range of tax cuts while keeping the US fiscal budget balanced. In Trump’s view, the implementation of tariffs is expected to raise massive amounts of government revenue to offset losses from reduced tax.

Source: Statista

However, Trump has likely underestimated the detrimental effects to US consumers including the impact of trade retaliation from Mexico, Canada and China. These are the three largest US trading partners, and we expect its effects to be felt far and wide.

Other avenues of budget reduction have been staff cuts by DOGE run by Elon Musk. We estimate to date DOGE has been able to reduce the government budget by US$ 400 billion which is a far cry from the US$ 2 trillion in cuts promised. More than 70% of the annual federal budget is represented by social security payments, Medicare and Medicaid. Any cuts to these programs directly affect the lowest income cohorts within the community. Excluding the large items, other material components of the budgets are defence spending and interest payments. Unless there are material cuts to any of these categories, it is unlikely that DOGE will be able to meet its stated objective.

We believe that the Trump administration will go ahead with the tax cuts which will further increase the federal costs. This will in turn result in an increase in government debt and translate into increased annual interest payments.

More concerning is the impact of the trade tariffs. Even under the best-case scenario where implemented tariffs are withdrawn, we believe the trade policy uncertainty will persist. We have seen evidence of companies delaying investment and hiring decisions. This will continue to weigh on growth over the medium term.

In the worst-case scenario of escalating trade tariffs, including retaliation by Canada, Mexico, China and the European union, we believe the impact to the global economy will be large. There are no winners in a trade war. In this scenario, we expect a short-term rise in inflation reflecting the passed-on costs of tariffs, followed by a large drop in output and consumption (effectively an economic recession).

Comparing the range of scenarios, we believe there is a wide dispersion of outcomes. Additionally, there is an added complexity of timing. The short-term economic pain for consumer does not necessarily mean a dire outcome for large multi-national companies who are likely to be more resilient. However, the evolution of trade policy (both US and trading counterparties) at this time is unknown and thus we prefer to maintain our market exposure within the portfolio.

| Asset Class | Portfolio Stance | Commentary |

| Domestic Equities | Neutral | We maintain a Neutral portfolio stance in Australian equities. Post the drawdown experienced in February and March, valuation for the asset class has started to look attractive, even adjusting for the potential earnings degradation. |

| International Equities | Neutral | We have maintained a Neutral position in International Equities; but within the asset class, have selected to maintain the marginal overweight to hedged International Equities (relative to unhedged). We believe the currency has moved too far and looks cheap from a valuation perspective. |

| Property and Infrastructure | Neutral | Property and infrastructure as an asset class have remained volatile and reactive to interest rates. Australian listed property remains a more concentrated market compared to global listed property. |

| Fixed Interest | Neutral | We maintain a Neutral portfolio stance. The evolution of trade policy, potential for economic recession and inflation have a wide set of implications for the asset class. In balancing both the upside and downside maintaining a neutral stance remains the prudent course of action. |

| Cash | Neutral | We have retained a Neutral cash allocation in our portfolios for buying opportunities should equity valuations reach attractive levels. |

In-line with the current outlook, the Investment Committee has elected to retain the Neutral portfolio stance, while maintaining our overweight to hedged international equities relative to unhedged. Focusing on the long-term, we are actively monitoring the equity market drawdown playing out today with a view of increasing our equity allocation should market valuation become compelling.

Allied Wealth Investment Committee

Allied Wealth's core principles

You are welcome to pass on this commentary or our contact details to anyone whom you think would benefit from our services.

Disclosure

The information provided in and made available through this document does not constitute financial product advice. The information is of general nature only and does not consider your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice.

We recommend that you obtain your own professional advice before making any decision in relation to your particular requirements or circumstances.

Allied Wealth Pty Ltd is a Corporate Authorised Representative of Allied Advice Pty Ltd for financial planning services. AFS Licence No. 528160