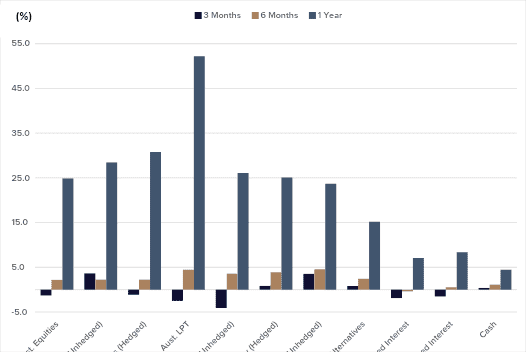

All asset class returns were positive over the 1-year period to October 2024; despite the marginal market drawdown experience in the month of October. Strong performance of Australian Listed Property over the year was primarily driven by the performance of Goodman Group which has an outsized allocation within the index.

Source: Allied Wealth, Morningstar.

Portfolios continue to maintain a Neutral asset class position; but with an overweight to hedged International Equities relative to unhedged. The relative currency position has been a strong return contributor over the September quarter; but has been volatile over the month of October. Outcomes of the US elections have implications for long-term monetary policy which make it difficult to take a directional view. Equity market valuations are expensive but can continue to rally further despite deteriorating consumer conditions. We provide further discussion on the outlook in the section below.

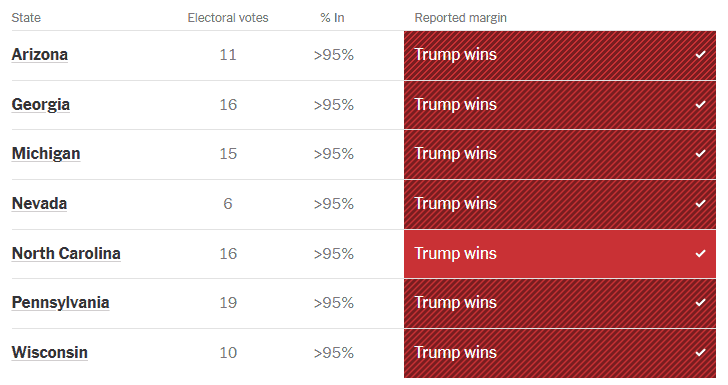

The US Elections concluded with a Republican win, and Donald Trump back in the presidential office for another 5-years. More importantly, apart from winning in all US swing states the Republican party won the majority across the US House of Representatives and Senate.

Source: NYTimes

Whilst the selection of key staff remains ongoing, President Trump has already indicated the key areas of focus are expected to be trade tariffs, tax cuts, government spending, immigration and border security – the first 3 have broad financial market implications. We provide some discussion points below.

We expect trade tariffs to be imposed on China at first, but will also be extended to Europe, Asia and Emerging Markets over time, with the primary goal of driving manufacturing back into the United States. However, implementation is expected to be disorganised given Trump’s temperament. The uncertainty is likely to weigh on corporate capital expenditure globally except for companies planning to relocate production back to the United States. Over the short-term, we do expect this to be beneficial for US growth but may result in materially higher inflation and interest rates over the longer term.

On the campaign trail, President Trump has floated several policy ideas including extending the Tax Cuts and Jobs Act, reducing corporate tax rates and exempting various income from income tax; all of which are stimulatory in nature. While the equity and equality of the proposed tax policy is debatable, the economic effects are stimulatory.

Proposed spending plans on the campaign trail has indicated that the US budget deficit is likely to increase by an estimated US$ 7.8 trillion under the Trump regime. However, the establishment of the Department of Government Efficiency (or DOGE for short) led by Elon Musk and Vivek Ramaswamy has promised more than US$ 2 trillion of savings via restructuring of government agencies, slashing regulations and dismantling government bureaucracy. It remains to be seen how this will shape out over the course of the next 5 years.

Despite the conclusion of the US election, we think there remains policy uncertainty. Over the short-term apart from tariffs on Chinese goods, we believe the economic impact from the election is minimal. Trajectory of US monetary policy in response to moderation in US (and global) inflation will likely be the key market driver over the short-term. We note across both developed and emerging markets, policy rates have been lowered and this is broadly positive for risk assets, incentivising more M&A activity.

Over the longer-term, the combination of extensive trade tariffs and government spending may have large inflationary implications in the US. This situation could be grim particularly if developed market central banks are forced to raise interest rates and trigger a rolling recession to battle runaway inflation.

For now, we have chosen to retain a broadly Neutral stance with an overweight in hedged international equities relative to unhedged. The Australian Dollar (relative to US Dollar and Euro), at current valuations still look cheap relative to history.

| Asset Class | Portfolio Stance | Commentary |

| Domestic Equities | Neutral | We maintain a Neutral portfolio stance in Australian equities. On a price-to-earnings basis, Australian equities look marginally overvalued relative to history, however the magnitude is not large enough to warrant a change in portfolio stance. |

| International Equities | Neutral | We have maintained a Neutral position in International Equities; but within the asset class, have selected to maintain the marginal overweight to hedged International Equities (relative to unhedged). |

| Property and Infrastructure | Neutral | Property and infrastructure as an asset class have remained volatile and reactive to interest rates. Australian listed property remains a more concentrated market compared to global listed property. |

| Fixed Interest | Neutral | We maintain a Neutral portfolio stance. The outcome of the US election is likely to have longer-term implications for the asset class. However, over the short-term, we expect more moderation in interest rates. |

| Cash | Neutral | We have retained a Neutral cash allocation in our portfolios for buying opportunities should equity valuations reach attractive levels. |

In-line with the current outlook, the Investment Committee has elected to retain the Neutral portfolio stance, whilst maintaining our overweight to hedged international equities relative to unhedged. We continue to monitor market condition but believe current positioning remains the most prudent course of action.

Allied Wealth Investment Committee

Allied Wealth's core principles

You are welcome to pass on this commentary or our contact details to anyone whom you think would benefit from our services.

Disclosure

The information provided in and made available through this document does not constitute financial product advice. The information is of general nature only and does not consider your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice.

We recommend that you obtain your own professional advice before making any decision in relation to your particular requirements or circumstances.

Allied Wealth Pty Ltd is a Corporate Authorised Representative of Allied Advice Pty Ltd for financial planning services. AFS Licence No. 528160