Asset Class and Economic Themes

In our last newsletter we highlighted a volatile market environment which has continued unabated. As the year has progressed, we have become resigned to the fact that volatility is here to stay. RBA cash rates are currently at 4.1% and this means that bonds once again produce yield. The impact of higher debt costs, combined with higher than target inflation prints, does introduce an increased level of future uncertainty – thus reflected in the volatile environment.

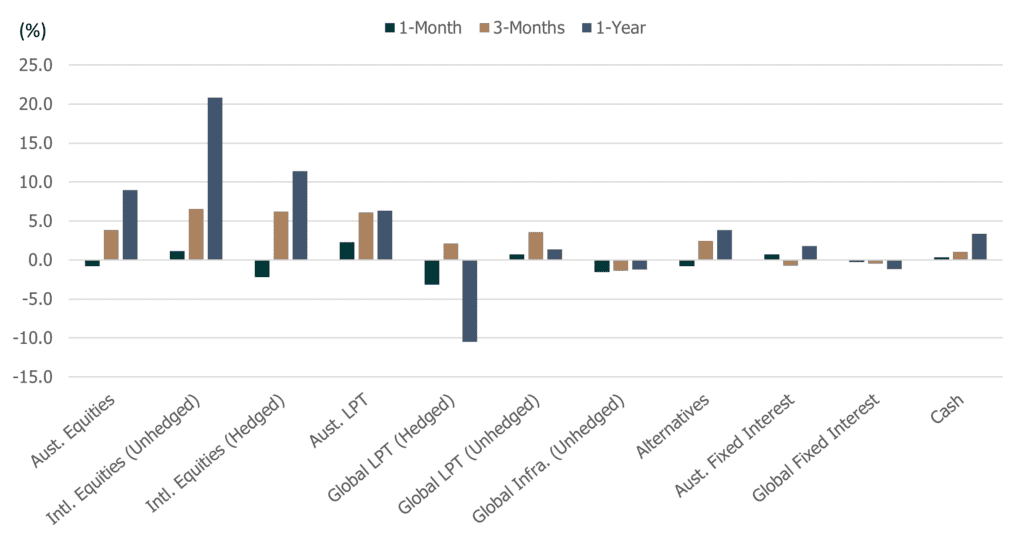

Whilst growth assets posted positive returns over the 3-month and 1-year periods, performance over the August month has been negative. The exception has been unhedged international equities which has benefitted from the depreciation of the Australian dollar, offsetting the negative equity returns.

Figure 1: Asset Class Performance as at 30 June 2023

Source: Allied Wealth, Morningstar.

Please note that asset allocation performance calculations have been conducted as of June 2023 and we will provide a further update to performance by the end of September 2023.

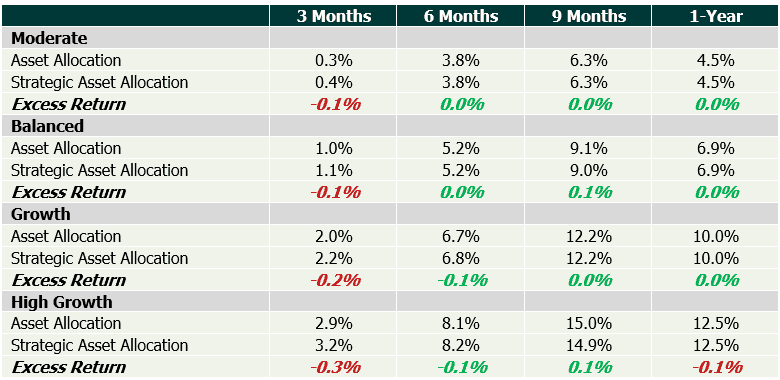

Portfolios currently maintain a marginally defensive asset allocation stance. As discussed in the last newsletter, the decision reflects a focus on risk management rather than profit maximisation. Whilst total return outcomes for clients are positive, our relative to SAA attribution indicates that this defensive position has detracted value over the June quarter as equity markets rallied.

Figure 2: Asset Allocation Performance as at 30 June 2023

Source: Allied Wealth, Morningstar. Note: Returns are based on an asset allocation index returns which do not include manager and advice fees so actual portfolio returns will vary. The purpose is to determine if our tactical asset allocation decisions are adding value over the Strategic Asset Allocation for each model.

What is Our Current Investment Outlook?

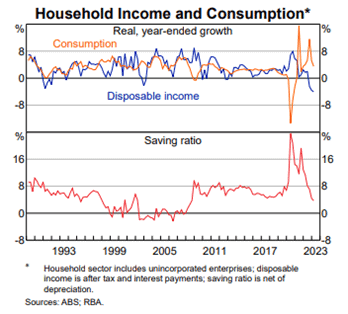

At the time of writing, the Reserve Bank of Australia (RBA) cash rate stands at 4.1% p.a. and represents an increase in interest rates by a whopping 4% since May 2022. The impact of higher interest rates has been felt by consumers; more so on the lower-income end of the spectrum. Higher mortgage payments and material increase in rents have eaten into the excess savings accumulated through the Covid19 pandemic and resulted in negative disposable income.

Figure 2: RBA Measure of Australian Household Income and Consumption

Obviously, this is not just a localised phenomenon. The same consumer impact is also observed in the United States (US). Despite tighter labour markets, wage growth has not outpaced the combined impact of higher inflation and mortgage rates.

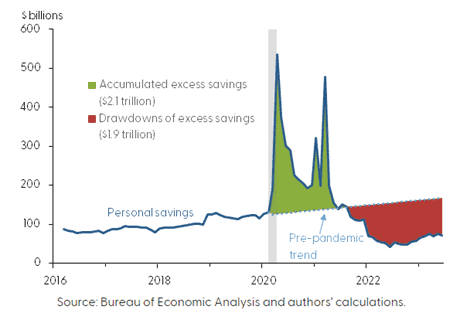

Figure 3: Consumers Aggregate Personal Savings versus the Pre-Pandemic Trend

Source: Federal Reserve Bank of San Francisco

From an inflation management standpoint, the sharp interest rate hiking cycle saw inflation ease over the last 6 months. In Australia, inflation peaked at 8% in December 2022, but since moderated to 6% in June 2023. Since the last rate hike in June this year, the RBA remained on pause but left the door open to further interest rate hikes if required. At 6%, inflation remains materially above the 2% to 3% targeted by the RBA.

Across July and August, companies domestically and globally reported on Q2 2023 earnings. Data suggests that earnings to date have remained resilient, but the forward outlook has been revised downwards. Costs management remains problematic for companies particularly as it relates to labour, rent and energy prices. Profit margins so far have been retained by passing on costs to consumers, and this in turn has contributed to the above target inflation number.

Ironically, labour cost pressures faced by companies is the reason why consumers have been able to broadly absorb the increased costs of goods. Consumers domestically face increasing cost pressures which is exacerbated by a large number of low fixed rate mortgages rolling off in August (termed the mortgage cliff). Anecdotally we believe the low-income cohort of consumers are already affected. In the most recent earnings season, Woolworths and Coles reported the highest number of grocery theft experienced in recent history.

Our base case remains that inflationary pressure is likely to stay above the targeted rate. This may mean another hiking cycle at the beginning of 2024. Timing of the interest rate hikes may occur at the same time labour market softens and when the majority of consumers have drawn down their pandemic savings. This is likely to lead to lower growth going forward which will in turn weigh on equity valuations.

What is the Counter to Our Investment View?

Whilst we have an investment outlook which reflects a negative view on growth assets, discussions held at the investment committee also included scenarios which would run counter to our base investment thesis. Following our analysis, we believe there are a specific set of conditions that will need to be met for equities to grind higher.

The key condition is that inflation continues to moderate over the forward period and comes in below the 3% upper band without any additional interest rate hikes. Additionally labour markets will have to soften but with increased labour productivity (i.e. people work harder for same level of pay). These two in combination will allow corporate profit margins to grow and justify current equity market valuations.

Despite our negative outlook, we acknowledge that both regulators and central banks have done a fantastic job at steering the economy over the last 12-months. We continue to expect them to utilise all the tools at their disposal to ensure any market downside is not permanent or long lasting.

Investment Market Trends

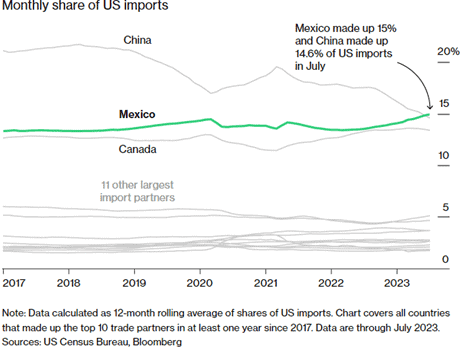

Outside of economic conditions, there have been two market themes that have captured our attention. Over the preceding quarters, we have written about how the geopolitical tension between US and China has resulted in a shift of factories and production away from China to US-friendly countries. We are finally seeing some concrete evidence to back this view. Trade data for the 12-months to July 2023 indicates that Mexico has now overtaken China as the largest exporters of goods to the US.

Figure 4: Mexican Exports to the US Finally Outpace China

Artificial Intelligence (aka. machine learning) has come a long way since its humble beginnings in 1956 when the first artificial intelligence (AI) program was presented at the Dartmouth Summer Research Project on Artificial Intelligence conference. Since then, we have seen substantial improvements to machine learning algorithms, data availability, computational power and costs of access such that machine learning models may be built and deployed by anyone with a personal computer and access to the internet. Thus, it is not surprising AI has taken over everything from creative endeavours to industrial manufacturing. Some machine learning models have even been deployed to support corporate decision making.

Even though we are very positive on the development of AI and its implications for humanity, we are concerned that AI has also become the marketing buzz word and the go-to panacea to resolve all our worldly ills. Take for example the claim that AI will solve global warming; whilst we can see how AI can help, ultimately a change in human behaviour will still be required to get there.

Selfishly, we are also getting a little tired of seeing AI slides in earning presentations promising the world. It would not be an exaggeration to say that 3 out of 4 earning presentations would include a slide dedicated to AI.

Investment Decisions and Strategy Implications

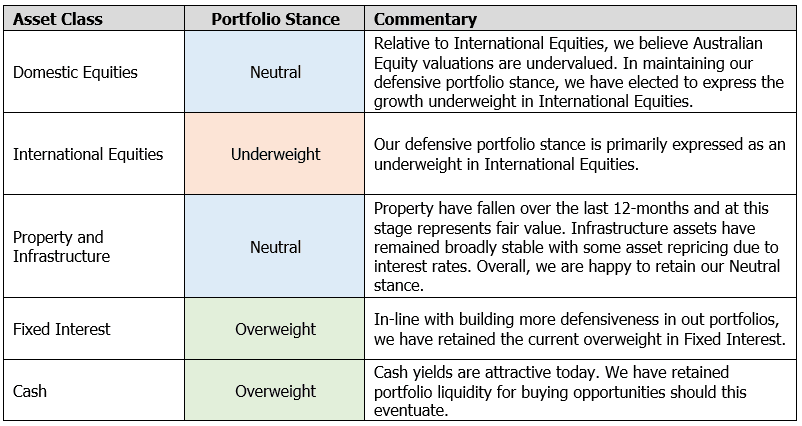

Coming back to our base investment thesis, given the confluence of events, we have made the decision to maintain a defensive stance across our portfolios. We believe there is stress building in the system despite the fantastic job done by regulators and central banks over the last 12-months. So far, the negative impact from the rise in interest rates has been broadly offset by substantial amounts of pandemic driven savings and tightness in labour markets – we do not believe this will last much longer. Despite the negative view, we are also monitoring the market for signs which are counter to our investment thesis. Emergence of a more positive macroeconomic environment may require a change in stance. From a risk management perspective, we remain comfortable with our current positions.

In-line with the outlook, the Investment Committee has decided to maintain an underweight growth assets in favour of an overweight to defensive assets. No asset allocation changes have been made.

Figure 5: Asset Class Summary and Portfolio Stance

Every investment decision is not undertaken lightly and is based on investment research, sized by our conviction. As with every decision we continue to monitor the market for signs of support or contradiction to our investment thesis.

Yours faithfully,

Allied Wealth Investment Committee

What sets Allied Wealth apart

Allied Wealth's core principles

You are welcome to pass on this commentary or our contact details to anyone whom you think would benefit from our services.

General advice warning

Disclosure

The information provided in and made available through this document does not constitute financial product advice. The information is of general nature only and does not take into account your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice.

We recommend that you obtain your own professional advice before making any decision in relation to your particular requirements or circumstances.

Allied Wealth Pty Ltd is a Corporate Authorised Representative of Allied Advice Pty Ltd for financial planning services. AFS Licence No. 528160