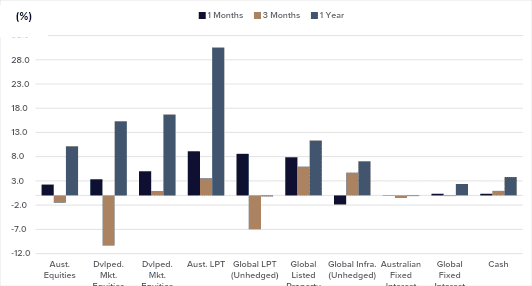

Asset class returns rebounded in April following drawdown in risk assets in March due to the Middle East conflict. Energy costs spiked as the conflict between US and Iran choked off the transport of oil via the Straits of Hormuz.

Source: Allied Wealth, Morningstar.

Coming into Q1 2026, economic growth remained positive while inflation conditions globally (excl. Australia) moderated. These relatively benign conditions were subsequently overshadowed by a sharp energy price shock and supply-side disruptions from the escalating conflict.

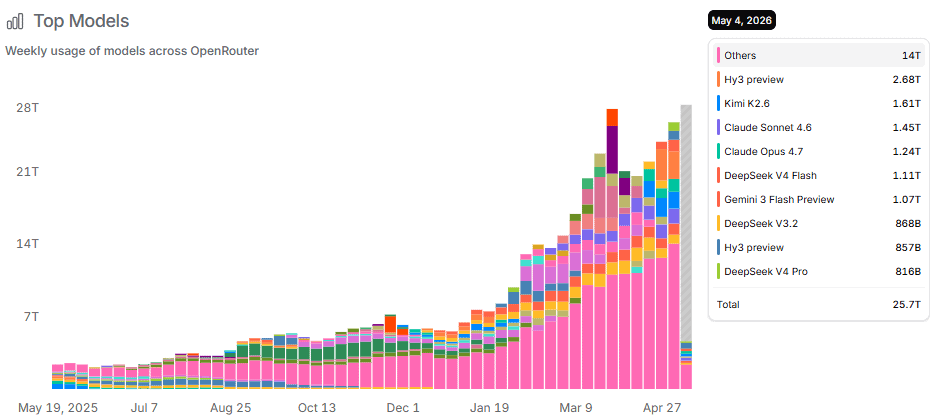

Since February 2026, investor sentiment toward technology and AI-related sectors has become more cautious, reflecting increased scrutiny of long-term earnings growth assumptions. We view the return of valuation discipline as constructive for the sector. At the same time, evidence of enterprise-level AI adoption is emerging (see AI-model usage in Figure 2), alongside development of real-world use cases at the software layer. This trend is corroborated by material revenue growth noted among leading AI model providers, including Anthropic.

Source: OpenRouter

Our assessment of this thematic suggests that, over the long term, corporations are likely to be the primary beneficiaries of AI adoption, with gains coming at the expense of consumers and segments of the workforce. Early data indicate that margin expansion is being driven by a combination of productivity gains and labour force rationalisation. While we do not expect immediate disruption to employment, we anticipate that the impact will emerge through structurally lower junior-level hiring, with potential implications for youth unemployment.

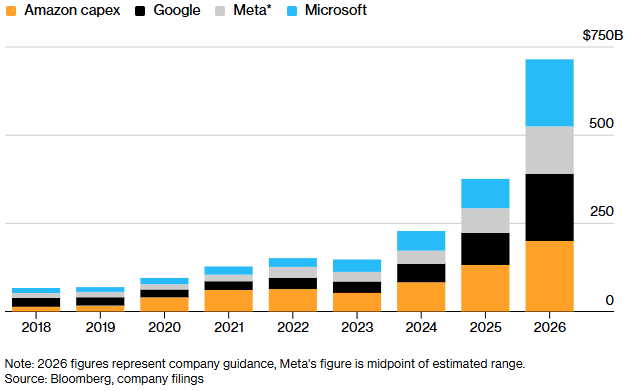

In contrast, elevated capital expenditure on data centres and energy infrastructure is expected to provide ongoing support to economic growth (Refer Capex by Hyperscalars in Figure 3 below).

In the Middle East, more than two months have passed since the conflict began. At the time of writing, an open-ended ceasefire remains in place with markets expecting a gradual re-opening of the Straits of Hormuz. It remains too early to tell at this point and the experience over the last two months remind us to expect the unexpected.

Despite the persistent tensions, we believe there are compelling incentives for all parties to pursue a negotiated resolution. For Iran, such an outcome would enable the continuation of oil exports and may facilitate broader economic benefits through potential sanctions relief. For the US, prolonged conflict and elevated energy prices carry growing political costs, particularly ahead of the mid-term elections scheduled for November 2026. Whilst the balance of incentives favours de-escalation, the timing remains uncertain. Until greater clarity emerges, equity and energy markets are likely to remain highly sensitive to regional developments.

Unlike many advanced economies, Australia experienced a re-acceleration in inflation even before the onset of the US-Iran conflict. This dynamic has been exacerbated by Australia’s structural dependence on Asian oil refineries, which themselves rely heavily on crude oil shipments from the Middle East, leaving domestic prices more exposed to external energy supply shocks.

In response, the Reserve Bank of Australia has tightened monetary policy aggressively, raising interest rates three times so far in 2026, with financial markets currently pricing in a further rise in August. Whilst these developments are likely to fuel a near-term lift in headline inflation, our medium-to-longer-term outlook remains consistent with a gradual moderation in price pressures.

This inflation episode differs materially from the post-COVID surge Australia experienced in 2022 and 2023. That period was characterised by unprecedented fiscal stimulus, severe supply-chain disruptions, and historically tight labour markets, which together resulted in persistent inflationary pressures. By contrast, current labour market conditions are materially weaker, with slower wage growth and easing employment momentum. These conditions reduce the risk that short-term price shocks translate into sustained inflationary pressures. Whilst inflation volatility is likely to remain elevated in the near term, the underlying macroeconomic backdrop suggests a lower probability of a prolonged inflation spiral.

Short-term economic growth is likely constrained by the energy-driven supply-side shock. However, we believe the structural drivers of long-term growth remain intact underpinned by sustained capital expenditure in AI and energy infrastructure. Additionally, we have observed clear evidence of enterprise-level AI adoption, supported by tangible use cases at the software layer. Our analysis suggests that corporates are the primary beneficiaries, with improvements in profit margins driven by productivity gains and workforce rationalisation, although this thematic is expected to unfold gradually over an extended period.

Following the recent market drawdown, equity valuations have become more compelling. Whilst short-term market volatility is likely to persist amid geopolitical risks, we believe current valuation levels offer an attractive entry point. Accordingly, we have implemented a modest increase in portfolio risk, expressed through an overweight position in international equities, funded by a corresponding underweight to fixed interest.

The Australian dollar appreciated over the quarter, with foreign exchange valuations now approaching fair value. While the historical overweight to AUD-hedged exposures has contributed positively to returns, we believe the more prudent approach at this juncture is to transition the portfolio to an unhedged AUD position.

| Asset Class | Portfolio Stance | Commentary |

|---|---|---|

| Domestic Equities | Neutral | We maintain a Neutral portfolio stance in Australian equities. The Australian economy remains more exposed to the energy shock compared to its global counterparts. However, valuations at this point are more attractive on a relative basis. Given the competing conditions, we prefer to maintain a Neutral stance. |

| International Equities | Overweight | We have moved to a marginal overweight position in International Equities. Long-term growth drivers remain intact and the recent market sell-off provides a good valuation entry point. Within the asset class, we have selected to remove the exposure to Hedged AUD as foreign exchange valuations are now trading at approximately fair-value. |

| Property and Infrastructure | Neutral | Property and infrastructure as an asset class have remained volatile and reactive to interest rates. Goodman Group represents almost 40% of the Australian listed property index. |

| Fixed Interest | Underweight | We have moved to an underweight portfolio stance. Given the inflation-related market shock, this asset class has experienced volatile trading conditions. The underweight also represents a funding position for International Equities. |

| Cash | Neutral | We have retained a Neutral cash allocation in our portfolios. |

Allied Wealth Investment Committee

Allied Wealth's core principles

You are welcome to pass on this commentary or our contact details to anyone whom you think would benefit from our services.

Disclosure

The information provided in and made available through this document does not constitute financial product advice. The information is of general nature only and does not consider your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice.

We recommend that you obtain your own professional advice before making any decision in relation to your particular requirements or circumstances.

Allied Wealth Pty Ltd is a Corporate Authorised Representative of Allied Advice Pty Ltd for financial planning services. AFS Licence No. 528160